The New & Old World of Credit

With credit for small business increasingly complicated, it is timely to revisit the guiding principles of credit. This will ensure that your finance application has the highest chance of success.

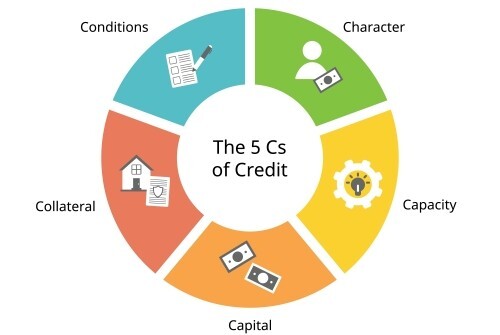

Banking credit and scoring models, from mortgages and small business lending through to corporate lending are complex, though in essence they draw back to fundamentals such as the the "Five Cs of Credit". These are:

Character, Capacity, Capital, Collateral & Conditions.

Simple perhaps, but timely for advisers and borrowers alike to keep in mind when dealing with credit providers.

Let's look at each of these, in the context of determining the level of risk associated with providing finance.

1/ Character

“Lending is not based primarily on money or property. No sir, the first thing is character.” J.P. Morgan

Character is best summarised as a borrower's willingness to meet their credit obligations. How trustworthy and reliable are they? In essence this is a "body of work" and something lenders ideally like to build an understanding of over time.

Of course, in the reality of assessing new lending scenarios, character is strongly weighted by credit reporting which is becoming increasingly sophisticated.

In short, without good credit character you won't move forward very far with the other Cs.

2/ Capacity

“If you would know the value of money, go and try to borrow some.”

Benjamin Franklin

We could devote pages just to Capacity. It may seem simple but borrowers do not always understand its importance in isolation.

Capacity measures historical, current and forecast cashflow, and the ability to repay debt obligations from these sources. Traditionally, assessing the risks of a commercial borrowing is more complex than a consumer or residential loan, but the latter is increasingly tougher too.

This is an area where borrowers find trouble and become frustrated with questions similar to: "I have so much collateral/security, so what is the issue for the lender?"

Yes, lenders want the option of multiple sources or retiring debt – cash, cash flow from business, asset realisation, or cash from an external source. Though the first way out through free cash is always the most desired. Lenders do not want to be forced to draw on assets or guarantors given the increasing level of compliance, uncertainty and adverse public relations that can impact their ability to do business.

This drives increasing levels of bank speak in mortgage applications or descriptive covenants in your business loans. Take Debt to Income Ratios in mortgages for example. More disclosure yes, but also an opportunity to build greater financial literacy for borrowers.

3/ Collateral

“One of the great responsibilities that I have is to manage my assets wisely, so that they create value.” Alice Walton

Collateral is often confused with Capital. Specifically, collateral is the assets that are pledged to support the loan. This provided a "second way out" for the lender after Capacity. This constitutes the traditional and tangible forms such as property or cash. It can also include specific or general cover over a business and its assets.

Collateral has been a big focus for mortgage and commercial lending. There has been a re-alignment around purpose of borrowing, and matching this to the appropriate collateral profile. For example, using a regulated mortgage product for business purposes is now a loophole that is closed. As are revolving lines of credit without a justifiable point in time purpose.

There are unintended consequences. This is contributing to a contraction in available debt in instances where new or emerging business have plenty of second way out, but not the first. So the days of starting a business with a dream and handing a property title to the bank are largely over.

The quality of the collateral provided does in turn drive risk and in turn, pricing. So we can't have it both ways. (Hence the growth of short-term financiers with interest rates like a phone book).

However, this will continue to find its level as the market becomes more developed and risks are better understood.

4/ Capital

“Capital is that part of wealth which is devoted to obtaining further wealth.” Alfred Marshall & Mary Paley Marshall

Often confused with Collateral. Capital is the value of assets that a borrower owns, which may include assets that are pledged as collateral for a loan.

Lenders like to see some contribution or "hurt" from the borrower and this is where a contribution of capital is desired, such as a material level of deposit for a property purchase, etc.

For example, a business or mortgage loan may be supported with a property given by a third party (guarantor) of considerable value but without any contribution of capital from the borrower. In this instance, there is a lot of collateral (second way out) but a lack of borrower contribution.

5/ Conditions

“Finance is not just about lending, it is about recovering loans also.” Raghuram G. Rajan

After the other "Cs" are met, the conditions of your loan kick in, such as the interest rate, the repayment term and the purpose of the money as critical factors. Commercial loans will have separate "covenants" which form part of the loan conditions.

The updated Banking Code of Practice talks of more "plain English". This should also help borrowers understand their obligations or any covenants that apply to their lending after it is funded.

The 5Cs in the real world

ABS data also tells us a story and gives a context (albeit crude) to the above discussion. Household wealth comprises $10.243 trillion in net worth. Made-up of $12.701 trillion in assets and $2.458 trillion in liabilities. So in a Capital sense this gearing looks ok.

Conversely, the ratio of household debt to disposable income has continued to increase, reaching a new historic high of 189.7%. So Capacity is being severely tested!

In summary, the more things change, the more they stay the same. Though the expectations across the Five Cs will intensify as the expectations of all the stakeholders in the credit process increase in the light of changing government policy.

For more on how to use the Principles of Credit for Better Outcomes, download our Business Lending Basics Guide.

Contact MCP

1300 510 816 or your Finance Partner

enquiry@mcpfinancial.com.au