June 2022: Rate Decision & Economy

The Reserve Bank of Australia ("RBA") met for June, raising the official cash rate by a further 0.50%.

There are more upward movements to come. It is a real challenge for the RBA - they need to lift rates to curb inflation but at a level and speed that does not put the economy into a sharp downturn.

Economic Results

The economic data was headlined this month with National Accounts that showed strong levels of private consumption, despite cost pressures.

So the economy is largely upbeat at the consumer end, with near 50 year low unemployment of under 4% supporting strong consumption. Spending ongoing is still supported by excess bank balances from stimulus which will keep the economy going to offset price rises.

Other parts of the economy, including business investment, are relatively weak. There is some concern that once the consumer's position weakens, the economy could drag too.

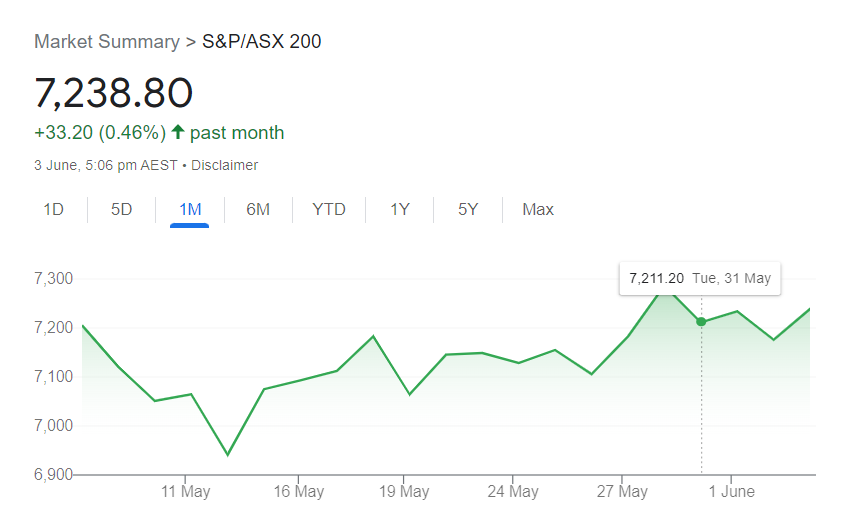

Shares & Markets

Over the month, the Australian share market was in the positive territory as indicated below:

The market was supported by gains mainly in materials and technology sectors.

The challenge facing companies is rising costs and potential limitations on growth may flow through to valuations at some point.

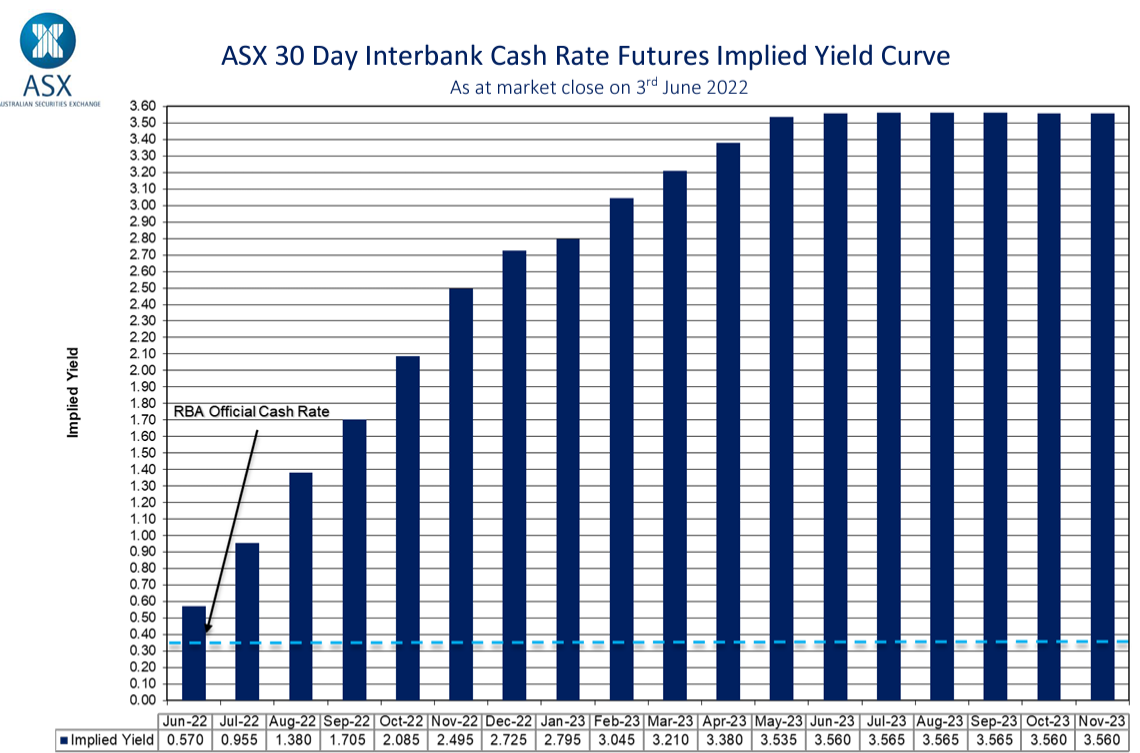

Direction for Local Interest Rates?

"It is appropriate to start the process of normalising monetary conditions." These were the words from our RBA Governor last month and the ride starts now.

How much the RBA moves from here is a little clearer.

Again, we draw our attention to the markets below. A rate increase in the medium term of more than 2.5% (or 250+ basis points). These predictions include indicators like the ASX Cash Rate Futures as below:

Looking at RBA commentary again, "The Board is committed to doing what is necessary to ensure that inflation in Australia returns to target over time. This will require a further lift in interest rates over the period ahead."

Fixed mortgage interest rates continued their rise, widening the gap between variable and fixed rates, however forecasts for the cash rate still look bullish.

Trends for Interest Rates Worldwide

The divergence in interest rate policy is significant. It is a chance for the RBA to go to school and watch how things evolve for different economies.

As a guide over the water, New Zealand raised interest rates by 0.5% to 2.0% in May. They have been a lot more aggressive than anticipated as they seek to control inflation and indications are that there is more to come.

“A larger and earlier increase in the OCR reduces the risk of inflation becoming persistent, while also providing more policy flexibility ahead in light of the highly uncertain global economic environment”, RBNZ governor Adrian Orr said. In other words, their strategy is to sprint it up and if relief (rate drop) is needed in the medium term, there is something to cut. Brutal but smart.

Across Asia, the strategy is very different. In China many lenders have recently cut interest rates, while Japan's Central Bank is keeping rates low by supporting the market by whatever means. At some point however, large differentials in rates will be a big problem.

In Europe, there are different issues at play. As a rule, movement in rates are less pronounced and rates sit well below the UK or US levels. In layman terms, many members of the Euro region have so much debt that even modest increases could put them on a knife's edge. That's a problem for strong countries like Germany, who would like an increase in interest rates for their local economy, but that means other weaker countries must do so too.

Money Markets

Another busy month on money markets, with an increase in short term yields still there but far less pronounced.

It may be a time where markets settle down a little.

| Month | Cash Rate | 180 Day Bill Rate | 10 Year Bond |

|

July 2021

|

0.10% |

0.07% |

1.48% |

|

August 2021

|

0.10% |

0.05% |

1.12% |

|

September 2021

|

0.10% |

0.04% |

1.18% |

|

October 2021

|

0.10% |

0.05% |

1.45% |

|

November 2021

|

0.10% |

0.20% |

2.09% |

|

December 2021

|

0.10% |

0.14% |

1.93% |

|

February 2022

|

0.10% |

0.26% |

1.98% |

|

March 2022

|

0.10% |

0.27% |

2.22% |

|

April 2022

|

0.10% |

0.70% |

2.87% |

|

May 2022

|

0.35% |

1.40% |

3.12% |

|

June 2022

|

0.85% |

1.60% |

3.48% |

The 180 day rate is another 20 points higher over the month, but has settled a little over the last few weeks. The yield curve steepened a little as the 10 year bond climbed by relatively more. Though again, there are early signs that this is settling down, albeit on a short amount of data.

In the US, the 10-year rate has been relatively settled for 6 weeks or so at around 3%. Stability right now is a good thing.

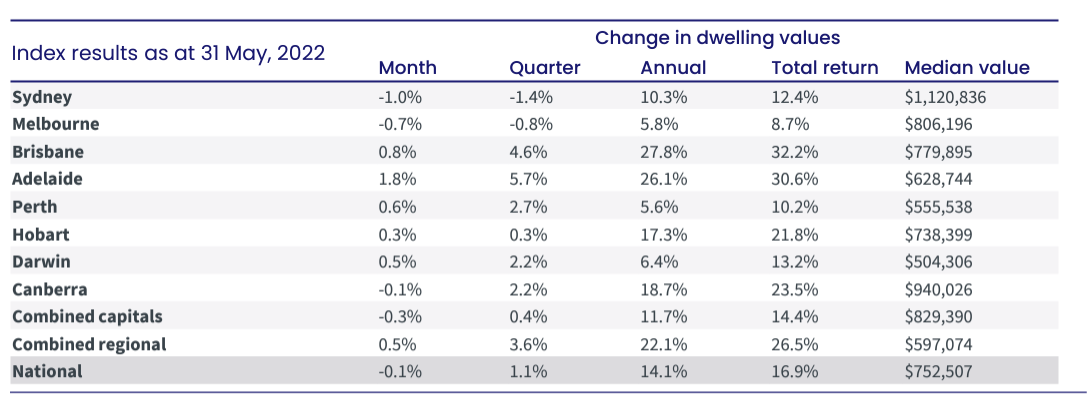

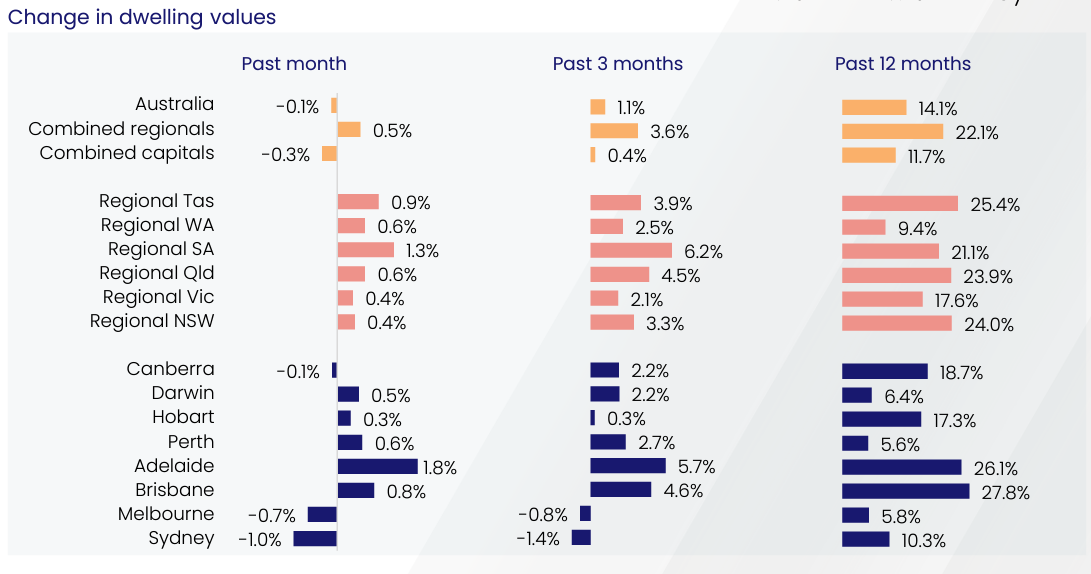

Property

Residential Property is continuing to level off.

CoreLogic data below shows the continued slowing of growth as the National Growth actually had red ink for the first time in a while.

Regional Properties holds its recent growth and is trending ahead of cities.

Commercial Property

According to data collated by Property Council of Australia, there was an increase in the number of workers heading to CBD offices across the country.

The data showed relative increases all around, led by Adelaide at 71% to just under 50% for Melbourne. Worth keeping an eye on these.

Currency

Who would be a currency trader. Currencies are all over the place at the moment. The Australian dollar actually strengthened this month against the USD - this was largely on the back of a weaker US dollar and its expectation of rate rises to come.

The relaxing of lockdown measures in Chinese cities was also a positive sentiment for our dollar's prospects.

Until next time.