May 2021: Rate Decision & Analysis.

The Reserve Bank of Australia ("RBA") left the official cash rate at 0.10% at its May meeting.

Despite an annual inflation result that was a little lower than markets expected, the overall conditions and sentiment in the economy are strong. In fact, the lower inflation results alleviates some concerns that activity in Australia was gathering pace too quickly.

U.S. economic data, specifically employment data and retail sales, was well on the upside of expectations. growing signs of global economic recovery amid a fast-tracking of vaccine rollouts and the passing of a US$1.9 trillion fiscal stimulus package by the incoming Biden administration

The latest NAB Quarterly SME Business Survey was further validation of improved conditions. Chief Economists Alan Oster said “The sectors which were most impacted by the pandemic continued to rebound in the quarter. Across all industries, Property, Finance and Health are now strongest – though all sectors are back in positive territory.”

Complimenting this, The Westpac-Melbourne Institute Index of Consumer Sentiment increased by 6% in April, which is an 11 year high. This helps us understand the momentum in the property market right now. (See Property below)

Saving (and borrowing) our Printed Money

RBA data is showing we have got a lot better at saving and repairing the household balance sheet. Households with a mortgage now have an average of four months' worth of expenses held back as savings.

Overall, the average household doubled their savings rate last year, to 12% of overall income. The savings rate is a good ting, though Governments want people to continue to spend too.

On the flipside, we are also borrowing more. Data from the ABS below shows the massive growth in mortgage lending with both low interest rates and a strong property market.

The U.S. Fed chairman, Jerome Powell, is really bullish about the US economy. “We feel like we’re at a place where the economy’s about to start growing much more quickly and job creation [will be] coming in much more quickly” he said. Hence the expectations of a 6.5% growth forecast for 2021, extraordinary times.

The pace of growth is also relatively strong in other developed economies but not at the same pace as the US.

Direction for Local Interest Rates?

The RBA retains a steady hand with their last month's board notes stating that the conditions required for a rate hike would not emerge until 2024 at the earliest.

As a result, there are still no expectations for any interest rate movements in the near term, though the momentum in longer term rates continues with both markets and lenders pushing up the cost of long term money.

For those calling the bottom, the argument is very compelling to support it.

Money Markets

Money Markets took a breather this month. The steady line in long term bonds, after the steady upward momentum during 2021, was actually a surprise to many economists, and a relief to others. Lower yields tend to reflect a more pessimistic outlook for growth, though it may also be the market doing a watch and see.

The numbers below are steady save for the tail off in the 10 year bond.

| Month | Cash Rate | 90 Bill Rate | 10 Year Bond |

| September 2020 | 0.25% | 0.12% | 0.84% |

| October 2020 | 0.25% | 0.10% | 0.90% |

| November 2020 | 0.10% | 0.05% | 0.81% |

| December 2020 | 0.10% | 0.05% | 0.90% |

| February 2021 | 0.10% | 0.03% | 1.09% |

| March 2021 | 0.10% | 0.04% | 1.69% |

| April 2021 | 0.10% | 0.05% | 1.74% |

| May 2021 | 0.10% | 0.04% | 1.65% |

The spread between short and long term rates will remain a crucial test of the market's view of the economy, including inflation, and the longer term direction of interest rate settings more broadly.

Property

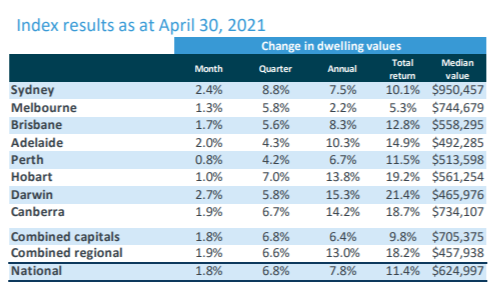

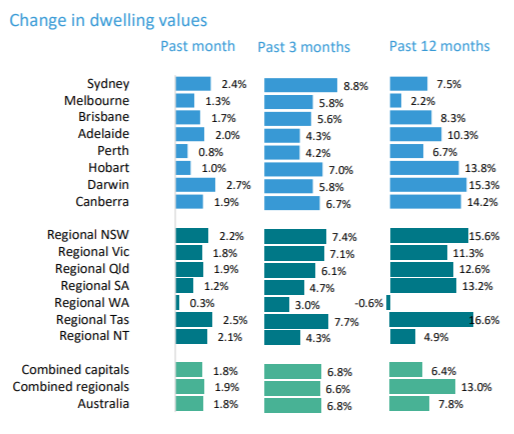

In the residential market, data from CoreLogic listed below, shows continued growth but finally at a lower level. National Growth was at 1.8% compared with 2.8% last month.

Annual returns remain very strong, with the smaller capital cities leading the way that have received a lot of interest from Sydney and Melbourne buyers.

There is naturally a lot of commentary about pace of capital gains could slow further over the coming months, as inventory levels rise and affordability constraints dampen housing demand.

Commercial Property

The commercial property sentiment remains solid. Investors are still chasing returns in an otherwise low yield environment.

The real story at the moment is Industrial property. As the data below from JLL shows, prime industrial yields are now lower than the yields on offices or retail. (NB: Yields being lower means that higher multiples of the property's income are being paid).

In a post Covid world, real estate investors are willing to pay a higher multiple (take a lower yield) for industrial assets as opposed to more traditional office or shopping centre investments.

As the JLL data above shows, the broader retail market is a mixed bag, and slowly we are seeing the impact of retail business that are unable to survive in an environment without Government support. This is started to show up in higher vacancy rates (more than 10% in many areas) and landlords will ultimately feel the pinch.

This may ultimately drive some material change in how retail property is delivered to the market.

Currency

The yo-yo of our currency continues, as markets pushed the Australian dollar back up this month. This was largely based on the strength of commodity markets as iron ore and copper prices continued their climb.

This increase was also against a stronger US dollar, as their economy rebounds at a faster pace than other markets including Europe.

Still, on the basis of these strong commodity prices continuing, experts still predict a rise back to 80c in the near term.

Until next time.