Credit is a critical element of a functioning economy. Whether you are a borrower, an independent finance broker or even a banker dealing with credit approvals, the approach to communicating your story is vital.

Increasing your Success Rate

Success in getting the support of a lender's credit department is about much more than just covering the Five 'Cs of Credit'.

To be clear, no amount of presentation or sophistication will mitigate a lack of acceptable 'Cs'; however, a credit submission that guides the reader to assess the key risks and mitigants will ultimately provide the best chance of success.

So, how should applications for business finance credit be structured?

Solving the Jigsaw Puzzle

To quote a senior credit manager; each business credit submission is like a jigsaw puzzle. Often, all the pieces are there, but they aren't well coordinated, explained, or coherent. There is no clear picture of what to build.

Credit Submission Format

Firstly, there is no set criterion for how long or detailed a credit submission should be. Submissions should not be seen as a badge of honour, nor should they look like a dog’s breakfast.

The key objective is to put yourself in the shoes of the recipient of the submission. Therefore, readability is paramount. Communicating important messages succinctly using bullet points and shorter sentences generally works well for the typical reader.

The supporting detail should be readily accessible, appropriately summarised and relevant to the key points you are communicating.

Understanding the Business & Industry

A critical starting point is to provide a thorough understanding of your customer. The business history, the owners' journey, the customers, suppliers, experience, key staff and of course existing banking relationships. This story will be unique to every customer.

From there, look at the industry in which the business operates.

What are the inherent risks? How are they relevant to your customer? Barriers to Entry? Where is the business in terms of its own cycle?

Identify these upfront, and explain succinctly the extent to which they apply and how they will be mitigated by your customer.

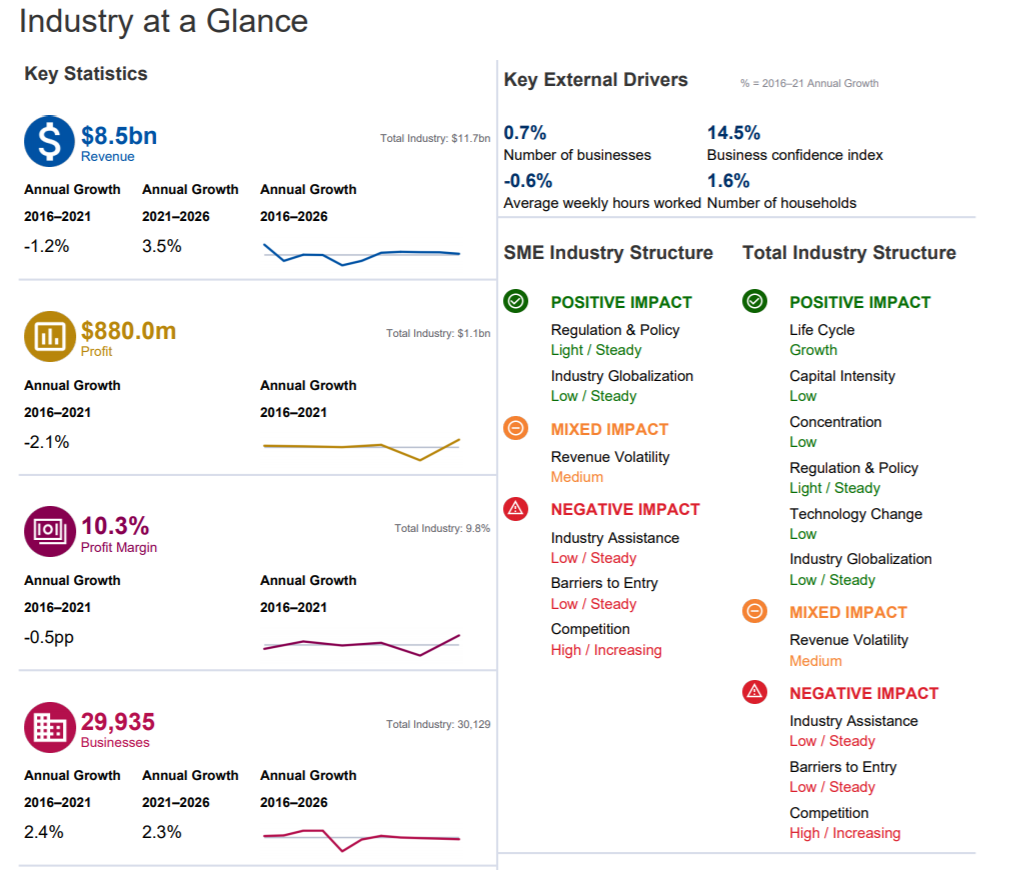

For example, let's say you operate in the Commercial Cleaning Industry. Industry data tools like IBIS World can help build a profile of your industry, as per the example below, extracting data on commercial cleaning.

The credit overview should deal with how your business compares with its industry. Put yourself in the eyes of the reader here, and take our cleaning example:

-

How do you ensure sustainability in an industry where there are typically low barriers to entry and a lot of competition?

-

The trend predicts low growth, so how will the business be different?

-

How does it relate to forecast results?

Presenting The Numbers

The historical financial performance is naturally very important, though the last completed financial statements may be many months old. Credit assessors will be more interested in the now and the future. What is happening now, and how does it impact performance?

Remember the old saying... Revenue is Vanity, Profit is sanity, but Cashflow is reality. Make sure you address the cash position and how it relates to the financial statements.

The business's Working Capital (WC) is an important factor, asit includes the profile of customers and suppliers, which is a critical part of understanding the business. It may not always be the most relevant component, but a good advisor will have great depth here to show that a review of the business WC has been completed.

Lastly, understand and communicate the quality of Management Information Systems (MIS), in an SME, as this can be very inconsistent in both structure and application.

Capacity is King, Capital is Comfort

The “first way out” for financiers is the cash flow from the assets they are lending against. Demonstrate clearly how the business can fulfil that requirement.

The ability to show this capacity can be complex. Financiers adopt different approaches, and they may not be transparent in how they assess this part. Though, as a general rule, you should show capacity to service debt on both a profit and cash flow basis. See our blog on Profit v Cashflow for more background here.

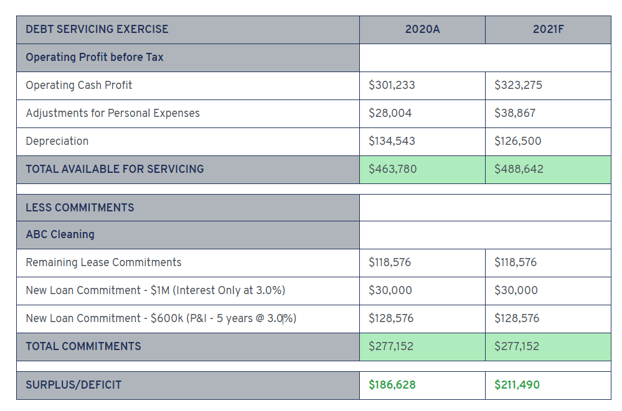

This is relevant to our Commercial Cleaning customer, where the cash commitment on Leases, for example, has a different profile to the expense in the Profit & Loss.

In our example, there is a reasonable operating surplus, which includes the new credit being sought.

Capital, or the “second way out”, is a comfort measure for lenders. Financiers want borrowers to be able to solve their own problems in times of financial distress, and a strong net asset position outside a business is a great mitigator.

Finally, after this is all done, the ultimate test is whether you would provide the funding based on your knowledge of the customer. If the answer is yes, then you're ready to send the submission for credit review.