October 2023: Rate Decision & Economy

The Reserve Bank of Australia (RBA) has today announced no change to the official cash rate, leaving it at 4.10%.

After a quiet month in August, any complacency around a period of consolidation was rocked by oil price spikes, currency and bond market adjustments. The softening inflation trend also saw a reversal.

There is suddenly fear around the stability of macro conditions, especially coming out of the US.

Economic Results & Sentiment

We got a reminder this month in why macroeconomic policy settings are so challenging. Despite the consumer really feeling the pinch, a surge in fuel prices was by far the largest contributor to inflation, after a rally in global oil, gas and refining prices that increased petrol prices.

As the consumer begins to feel more pressure on their cash flows, the policies to curb inflation can also hurt the consumer.

Australian Bureau of Statistics’ (ABS) data showed the annual inflation rate rose to 5.2% in August, from 4.9% in July, which was broadly within expectation but still rocked markets. After oil and petrol, price pressures included jumps in the cost of food, housing and transport.

Offsetting the consumer softness is that employment data remains strong. There are sustained high levels of job advertising and vacancies with an additional 64,900 jobs added in August.

Consumer Savings Reverse

There were the first signs that consumers are dipping into savings from the COVID-19 money dump. ABS data showed the first fall in deposit balances since the GFC 15 years ago. This implies that households are tapping into cash reserves to support cost of living.

This of course doesn't make retailers happy, regardless of what is happening in "macroeconomics".

RBA Stance

With the hold at September's meeting, the RBA commentary is still robust on inflation and the current data will reverse its softer tone a little, a challenge for the new Governor.

“Some further tightening of monetary policy may be required to ensure that inflation returns to target in a reasonable timeframe, but that will continue to depend upon the data and the evolving assessment of risks.”

Shares & Markets

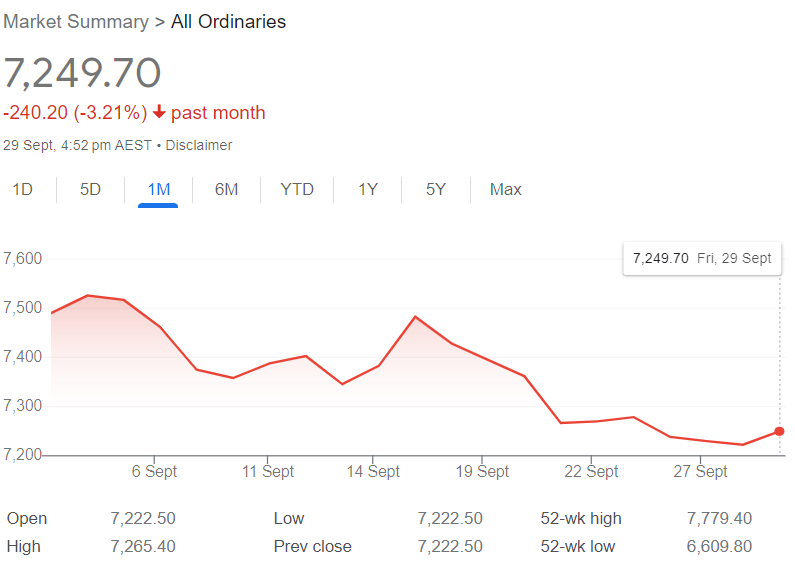

Overall, the market ended September with a fall in the All Ordinaries, continuing the losses from last month.

The broader sentiment around expected sustained interest settings, rising oil prices amongst other uncertainties dragged markets down. While markets offshore were harder hit, the Australian market was cushioned a little by stronger commodity prices including iron ore.

In the US, September has maintained its trend as being a weak period for equities. Their markets having a loss of circa 4% over the month. US equity markets have shown resilience especially with the bond market's volatility. For example, despite the recent falls from mid year the S&P 500 is still up 12% this year.

Many believe that this is not sustainable and something may have to give.

Direction for Local Interest Rates?

We often talk about the diverging views of "The Market" and "The Economists". The obvious divergence in behaviour is speed.

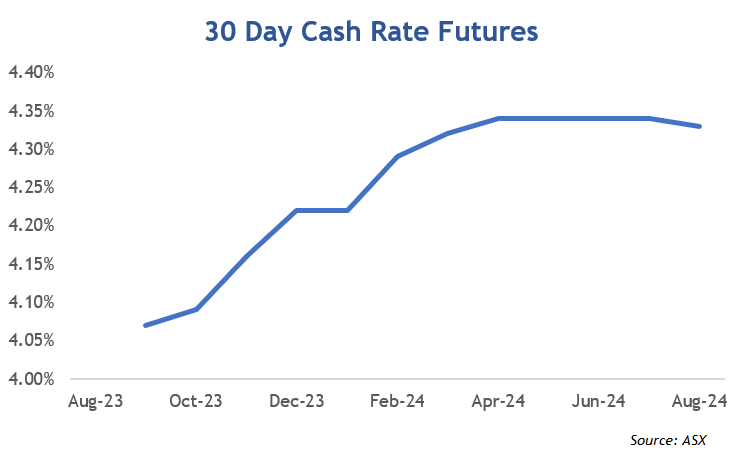

Movement in the ASX Cash Rate Futures offers some insight. This month, the shape of the curve changed (again), with a 25 point increase in expectations. The market is no longer seeing interest rates being at the peak of the tightening cycle.

This is indicated by the ASX Cash Rate Futures as below.

Financial markets are now implying that the cash rate will trend up early in 2024 and then settle a little. This reset catches up to many Economists maintaining that more tightening of monetary policy was possible.

Perhaps this will also satisfy the many voices that cannot see such a sustained divergence in US and Australia cash rate settings.

Update for Interest Rates Worldwide

As a broad statement, Australia is clearly more patient than the rest of the world in allowing inflation to take longer to come back to target range. Most countries aren't so prepared to wait it out.

New Zealand's central bank left the cash rate unchanged again at 5.50%; however signaled that the risk on inflation remains and the market should not be surprised at further tightening. They are very clear in their message of "whatever it takes" to curb inflation.

In the UK, the Bank of England made their first pause in rises since December 2021, keeping rates at 5.25%. Despite this pause, most are expecting more tightening to come.

The U.S. held the 5.50% rate at their last meeting, amongst much noise in the economy. Fed officials are staying the course and do not want to end monetary tightening early, especially with surging oil prices putting strong upward pressure on inflation. The sobering news for some is that majority of Fed committee members see their cash rate still above 5% by the end of 2024.

Canada, stays at 5.00%, and their markets are not pricing in any rate cuts to 2025.

Central Bank Cash Rates

Before posting any changes today we compare central bank cash rates and their longer term 10-year bond yields.

With little movement in central cash rates, the spread in most countries is now less inverted with the increases in 10 year rates. Australia is now "in the black".

|

Country |

Cash Rate | 10 Year Bond | Spread |

|

Australia

|

4.10% | 4.48% | 0.38% |

|

Canada

|

5.00% | 4.07% | -0.93% |

|

China

|

3.45% | 2.71% | -0.74% |

| Germany | 4.50% | 2.85% | -1.65% |

| India | 6.50% | 7.21% | 0.71% |

| Japan | 0.00% | 0.75% | 0.75% |

| New Zealand | 5.50% | 5.39% | -0.11% |

| Singapore | 3.71% | 3.15% | -0.21% |

| United Kingdom | 5.25% | 4.46% | -0.79% |

| United States | 5.50% | 4.58% | -0.92% |

The overwhelming view of the market is that longer term rates are likely to continue as inflation remains firmly settled in.

Local Money Markets

Australian money markets followed the bond market sell off and all the action was at the long-term end of the curve. The 10-year rate spiked almost 50 points after the jolt of rising oil prices and expectations of higher rates for longer.

| Month | Cash Rate | 180 Day | 10 Year |

|

Oct 22

|

2.60% |

3.55% |

3.90% |

|

Nov 22

|

2.85% |

3.61% |

3.74% |

|

Dec 22

|

3.10% |

3.48% |

3.48% |

|

Feb 23

|

3.35% |

3.67% |

3.50% |

|

Mar 23

|

3.60% |

3.94% |

3.85% |

|

Apr 23

|

3.60% |

3.81% |

3.30% |

|

May 23

|

3.85% |

3.82% |

3.34% |

|

June 23

|

4.10% |

4.21% |

3.65% |

|

July 23

|

4.10% |

4.67% |

4.03% |

|

Aug 23

|

4.10% |

4.70% |

4.06% |

|

Sep 23

|

4.10% |

4.37% |

4.02% |

|

Oct 23

|

4.10% |

4.41% |

4.48% |

Nothing like market volatility to flatten the yield curve.

Residential Property

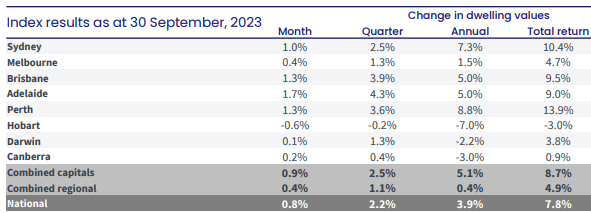

The latest residential monthly property results from CoreLogic showed a better than expected level of growth.

The increase is a seventh consecutive monthly rise against a smaller level of listings and there is diversity in the results again. With Adelaide, Perth and Brisbane leading the charge in the "middle" of the value curve, these cities are at all time highs. The next few months will be interesting.

Commercial Property

A lot of the excess supply in commercial property is not hurting prices at the lower end and there are a number of emerging trends.

Firstly, the rise in interest and vacancy rates is discouraging investors, but a lot of owner occupiers are taking advantage of the resultant falling competition.

Secondly, according to a number of agents, there is a growing trend of corporates and SMEs taking higher quality space in superior locations though with a significantly smaller lettable area. This includes a shift into inner city fringe close to transport.

Others looking to the very long term are seeing, like residential, that a lack of new projects being marketed may lead to scarcity in the longer term.

Currency

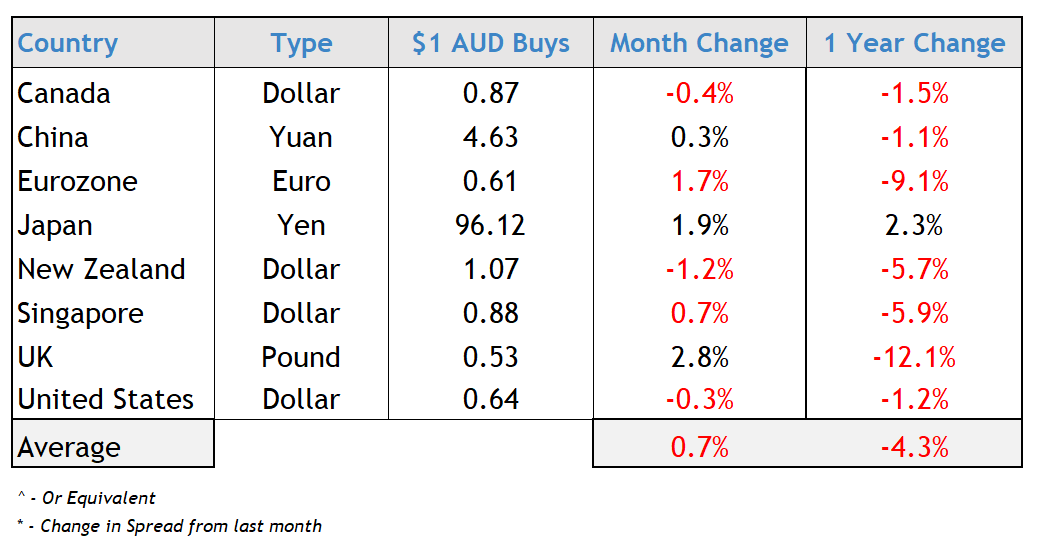

The Australian dollar lost ground again against the majority of other currencies, other than the Japan and UK currencies. In relation to the USD, it got hammered early in the month before a rally back on the sentiment of Australia's higher interest rates for longer outlook.

The USD has become the investment destination for cash, whereas historically the stable economies of Australia and New Zealand offered a premium which drove demand for their currency. New Zealand still offers that, but for now and the foreseeable future, this is no longer the case in Australia.

Again, a sustained weaker currency is causing headaches for importers and is a niggle in the battle to control inflation. The opposite is also true as Australian assets are cheaper which helps support property, business and equity markets.

We hope that the month ahead brings you prosperity and success.