December 2022: Rate Decision & Economy

The Reserve Bank of Australia ("RBA") met today for December, raising the official cash rate by a further 0.25%. This was a tighter call than it would have been earlier in the month.

Economic Sentiment

Inflationary fears were on hold last month. Australia’s CPI slowed to 6.9% in the year to October, well below expectations and down from 7.3% from last month.

It is an early call, but the data suggests that inflation could be reaching a peak. This was led by some encouraging signs in markets like Germany which had a decent dip too. All markets are responding quickly to any signs about the direction of inflation and interest rates.

The RBA Apology

Interesting one during the month, enduring the Senate economics committee ripping into the RBA board and Governor Dr Lowe.

The Governor did give an apology to those affected, but stating they did not expect the conditions for change to be met “until 2024 at the earliest”.

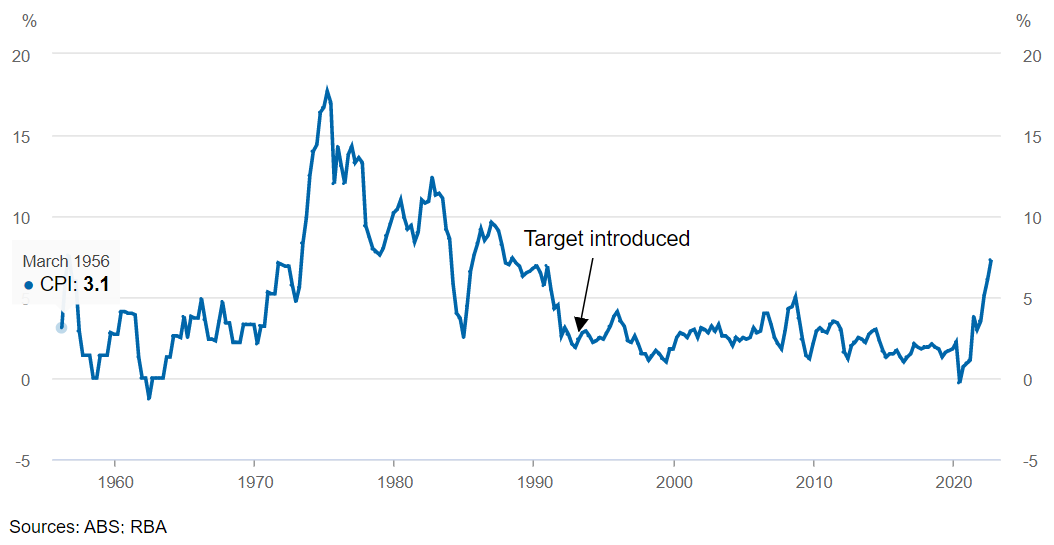

Hindsight is a wonderful thing. In a world where people are screaming for direction and leadership, the RBA did attempt to provide some clarity in how they saw things. There are no guarantees and we have included the graph of inflation growth from last month again below to show how quickly things can change.

Not sure what is gained from the blame game. Always better to focus on the solutions.

Local Results

Whilst the step down in inflation growth was well received, there is caution including from the Treasurer. “The October result is yet to fully reflect the impact of the floods on grocery prices or the hit to energy bills caused by the war in Europe,” Dr Chalmers said.

Employment remains really strong, with unemployment levels at only 3.4%. On the other side, investment in business - reflected in lower plant and equipment purchases so some signs of softness.

Shares & Markets

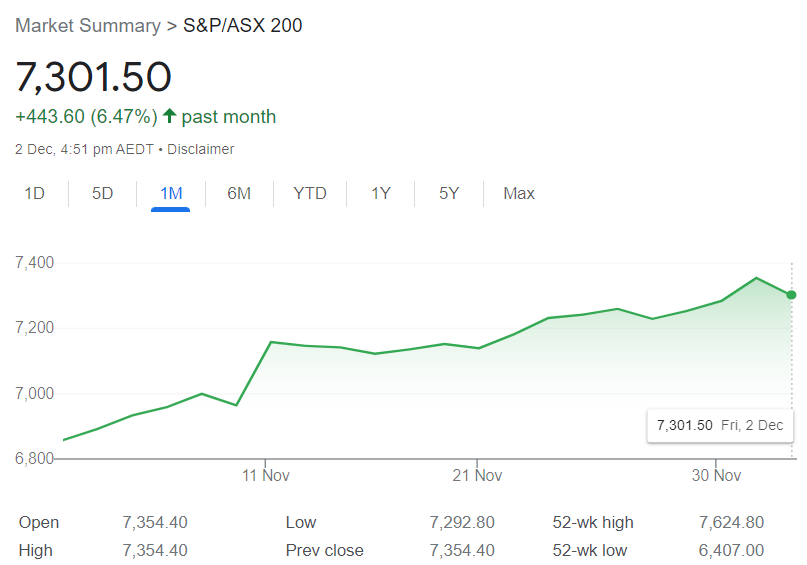

For the second month in a row, the Australian share market had a positive month, rising by over 6%. Markets touched a seven-month high during the month, with dips during the current tightening cycle all but wiped out now. Why? Well it is a reminder that current economic data isn't aligned to market performance, and future expectations are the key driver.

Wall Street’s S&P 500 index continued its strong growth. The release of strong employment data gave momentum along with the early signs that inflation could be tapering off a little.

Direction for Local Interest Rates?

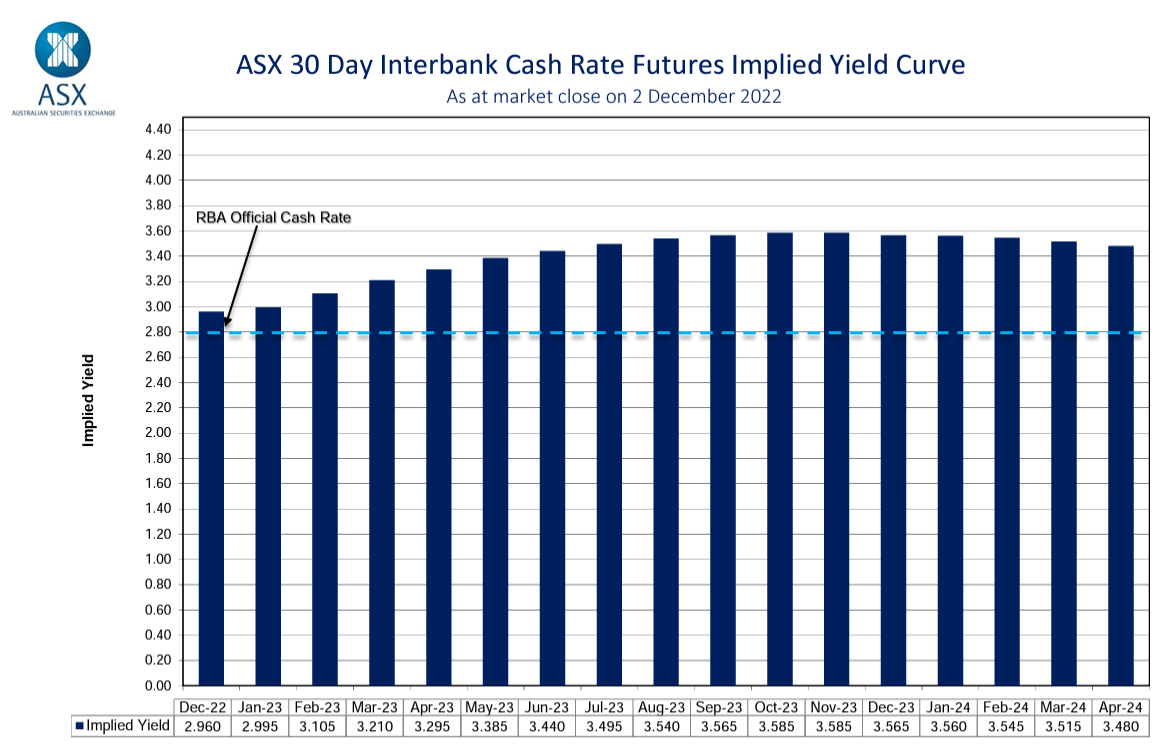

Again, some insights from the ASX Cash Rate Futures, gauging month to month expectations in terms of a destination for the peak cash rate. We held the view that market had overcooked things a little, but a 40 basis point or so (0.40%) dip from last month is still a strong drop.

Now a little under 3.60% by early 2024,as indicated by the ASX Cash Rate Futures as below.

As with bond rates, we expect wide fluctuations with this data in the coming months.

Update for Interest Rates Worldwide

Central banks across the developed world are now managing their interest rate strategy a little differently. The recriminations have started, with "experts" saying that rate rises did not happen soon enough and there was too much money printed etc.

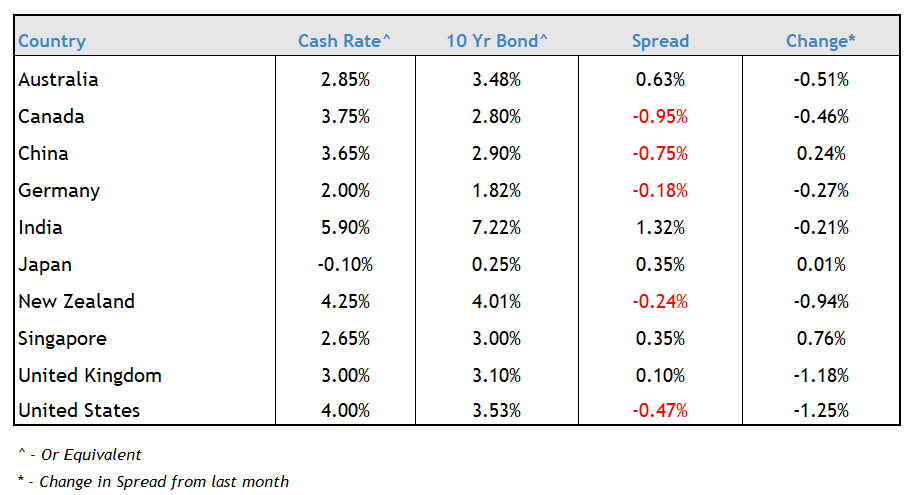

New Zealand's central bank brought out the baseball bat and raised interest rates by another 0.75% to 4.25%. There remains some concerns around the speed of tightening, and the long term bond market shows that. However, inflation is running at 7.2%, well above its target rate.

A recent review of the central bank, yes with hindsight, stated they were too late in raising rates in late 2021 though it is not clear the end destination would have been any different. Some real challenges continue there and they clear about taming the inflation beast, recession or not.

In the UK, the Bank of England in response to rampant inflation - now expected to peak at 10.9% - delivered an increase by 0.75% to 3.0%, the largest single lift since 1992. Though unlike the US, NZ and others, their tone was much more conservative for going forward. Time will tell who is right.

In the U.S, The Federal Reserve has made some dampening comments on rate increases, though they are still looking at a 50 point increase at their mid December meeting. “The time for moderating the pace of rate increases may come as soon as the December meeting,” Mr Powell said giving confidence to markets that tightening is starting to slow.

In Canada, their central bank is expected to deliver another 50 point hike this week, before pausing in 2023. It will either need to or markets will have to adjust, as their yield curve is looking crazy.

Japan keeps its policy rate unchanged at minus 0.10%, no changes are expected and maybe they can hold out until this cycle reverses! Or their currency bottoms out.

Following on our data from previous months, and again before posting the change today, we compare central bank cash rates and their longer term 10 year bond yields. The "spread" has moved widely as cash rates are climbing and long term rates are heading the other way.

The market is saying we are reaching the peak, with future economic conditions that will force a retreat in monetary policy over the longer term.

Money Markets

Australian money markets in November have been absorbing trends from around the world and the expected reduction in the size of cash rate increases.

It is a very flat yield curve right now.

| Month | Cash Rate | 180 Day | 10 Year |

|

Dec 2021

|

0.10% |

0.14% |

1.93% |

|

Feb 2022

|

0.10% |

0.26% |

1.98% |

|

Mar 2022

|

0.10% |

0.27% |

2.22% |

|

Apr 2022

|

0.10% |

0.70% |

2.87% |

|

May 2022

|

0.35% |

1.40% |

3.12% |

|

Jun 2022

|

0.85% |

1.94% |

3.48% |

|

Jul 2022

|

1.35% |

2.70% |

3.54% |

|

Aug 2022

|

1.85% |

2.78% |

2.96% |

|

Sep 2022

|

2.35% |

3.04% |

3.65% |

|

Oct 2022

|

2.60% |

3.55% |

3.90% |

|

Nov 2022

|

2.85% |

3.61% |

3.74% |

|

Dec 2022

|

3.10% |

3.48% |

3.48% |

The 180 day rate tailed down over the month, due to a softening around rising interest rate expectations.

The 10 year rate had wild mood swings during the period, but the trend followed 3 and 5 year rates in heading down with expectations of moderating inflation and interest rate hikes. A tough time for anyone trading actively in markets.

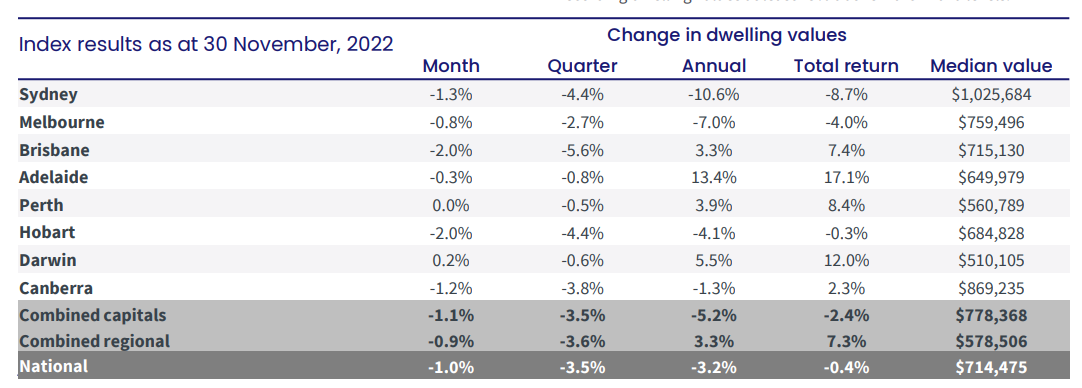

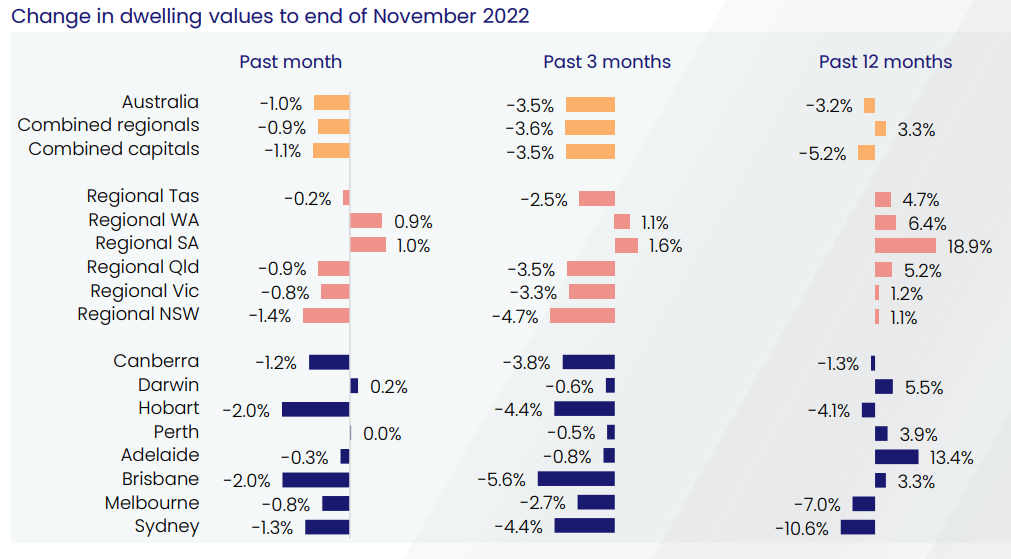

Property

The latest residential monthly property results from CoreLogic show a continuing decline and the previously rising markets are now coming off. (Brisbane, Hobart).

The number of listings remained down on the same time last year, this may be contributing to a slowdown in falls in both Sydney and Melbourne. The coming months will be interesting.

Commercial Property

This property class is obviously not as fluid as residential, with transactions limited while the market works out what the new normal looks like.

Vendor and purchaser expectations therefore remain a long way apart which explains why volumes are so low. For borrowers, we are seeing first hand that it is very tough to show an ability to service interest repayments using the property's income as the sole source.

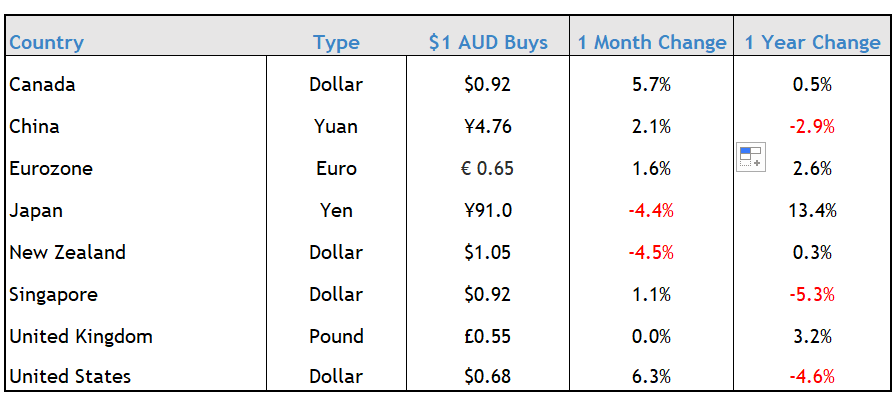

Currency

The Australian dollar rallied this month against the USD at around US68¢.

Considering our cash rate is at a lower level than other developed economies, the performance below is very strong and is supported by strong commodity prices.

Relative interest rates in New Zealand for example are now very wide, which explains the stronger NZ dollar against the AUD.

For people or businesses reliant on overseas goods and services and battling cost pressures, this is a welcome direction.

We wish you a very happy lead in to the close of 2022.