November 2022: Rate Decision & Economy

The Reserve Bank of Australia ("RBA") met today for November, raising the official cash rate by a further 0.25%.

Economic Sentiment

Inflationary fears are still driving sentiment. Locally, nominal inflation increased 1.8% in the September quarter taking the annual rate to 7.3%, which was beyond market expectations and making things more challenging for interest rate settings.

The numbers are not pretty across the board. Take the Eurozone for example, with nominal inflation in Germany and Italy just under 12%, and the US where inflation is stronger than Australia.

There are a number of traditionally negative signs emerging; stronger US currency, inverse yield curves etc. that we walk through below.

Local Results

Last month we talked about a slight improvement with inflationary targets, and the hope that Australia’s inflation rate is not growing. However, the current results were led by rising gas and construction costs, amongst other essentials. The recent floods across Australia will add more inflationary pressure too, expected to lead to near 10% price increases in food prices over the next six months.

Despite the upward pressures, many economists are still cautioning that rising prices need to be considered in the context of a weakening global economy.

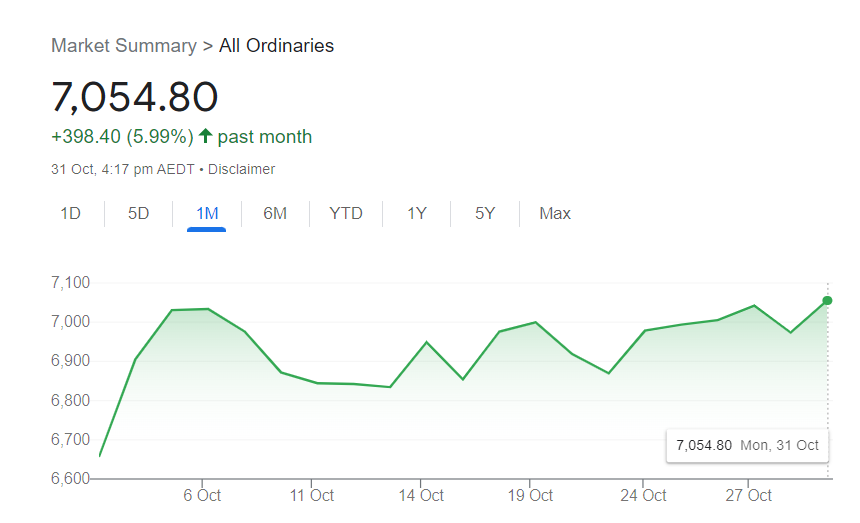

Shares & Markets

For the first month in a while, the Australian share market had a good month, rising by 6%. The RBA’s surprise in October with only a 25 basis point increase was a positive for markets. The strong inflation result drives sentiment the other way so it is a tightrope at the moment.

Wall Street’s S&P 500 index has risen 9% over the last few weeks, a real rally. The release of US employment data this week will be another guide for markets looking for direction.

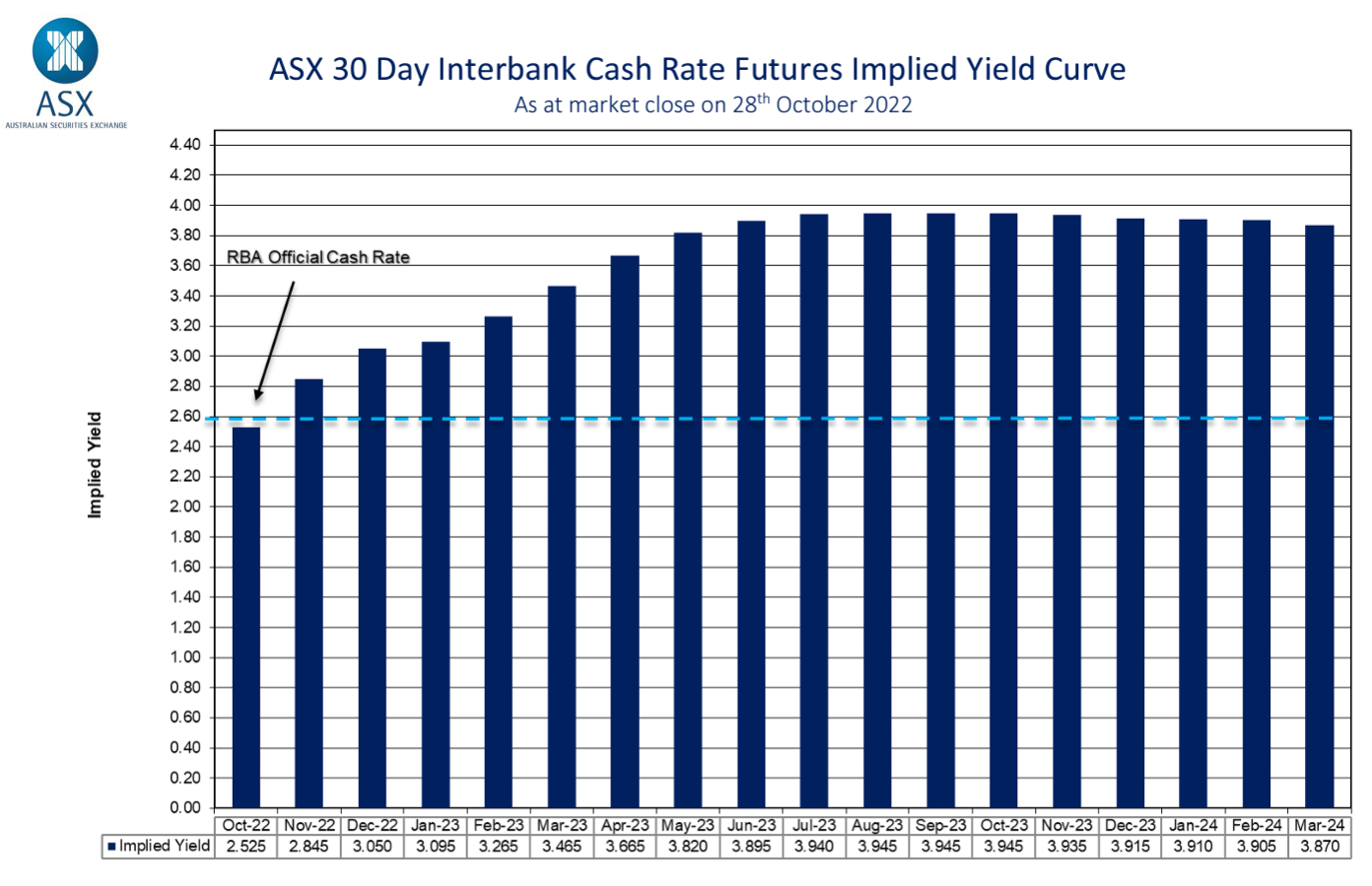

Direction for Local Interest Rates?

Again, some insights from the ASX Cash Rate Futures, gauging month to month expectations in terms of a destination for the peak cash rate. Last month's lower than expected rise was against market expectation, so is a 10 basis point or so (0.10%) dip from last month as indicated by the ASX Cash Rate Futures as below.

Now a little under 4.0% by early 2024, as shown below.

World economic events are largely driving this outlook. The RBA's resolve will be tested if other key local indicators soften.

Update for Interest Rates Worldwide

Central banks across the developed world are now increasing interest rates with relative consistency.

New Zealand's central bank raised interest rates by another 0.50% to 3.50% as expected. There are some concerns around the speed of tightening, however the market is still expecting another 0.5% rise at the next central bank meeting.

In the UK, the Bank of England continued buying long term bonds. Most economists think that rates will rise by 0.75% to 3.0% when they meet later this week in a time where recessionary fears take hold.

In the U.S, The Federal Reserve still hasn't put a ceiling on rate increases, The Federal Reserve holds its policy meeting this week, where it is expected to raise its central interest rate by 0.75% to 4.0%. This will meet expectations, but the market will be looking for leadership in their commentary.

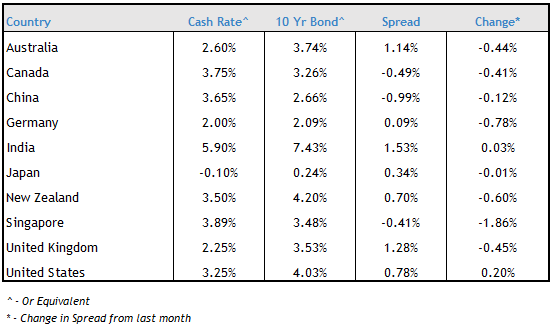

In Canada, their central bank surprised markets with a rate increase of "only" 0.5% to 3.75%. The comments indicated that their strong stance in lifting rates was starting to impact, and policy matters are looking at longer term impacts. The market agrees as their yield curve is now inverted (see below).

Japan keeps its policy rate unchanged at minus 0.10%, no changes are expected in the short term much to the surprise of some.

Following on our data from last month, and before posting the Australian change today, we have included a listing of central bank cash rates and their longer term 10 year bond yields. This is far from a perfect science, but a blunt gauge on sentiment between a country's short and longer term rate settings. Not surprisingly, the "spread" has narrowed as cash rates are climbing (e.g. US, UK & NZ spread will be largely knocked out shortly).

It does send a message about market expectations around aggressive increases, followed by a likely economic stagnation that will force a halt or retreat of tightening monetary policy over the longer term.

Money Markets

Australian money markets in October shocked fixed income markets with the RBA's reducing the size of cash rate increases to 0.25% from the 0.50% expectation. It took the month for rates to play catch up.

So, we were out of step with the rest of the world, but the result was a stable start and end on the markets.

| Month | Cash Rate | 180 Day Bill Rate | 10 Year Bond |

|

November 2021

|

0.10% |

0.20% |

2.09% |

|

December 2021

|

0.10% |

0.14% |

1.93% |

|

February 2022

|

0.10% |

0.26% |

1.98% |

|

March 2022

|

0.10% |

0.27% |

2.22% |

|

April 2022

|

0.10% |

0.70% |

2.87% |

|

May 2022

|

0.35% |

1.40% |

3.12% |

|

June 2022

|

0.85% |

1.94% |

3.48% |

|

July 2022

|

1.35% |

2.70% |

3.54% |

|

August 2022

|

1.85% |

2.78% |

2.96% |

|

September 2022

|

2.35% |

3.04% |

3.65% |

|

October 2022

|

2.60% |

3.55% |

3.90% |

|

November 2022

|

2.85% |

3.61% |

3.74% |

The 180 day rate was again volatile over the month, especially with speculation around changing interest rate expectations.

The 10 year rate might have started and finished not far apart but again there were wild mood swings during the period. A tough time for anyone trading actively in markets.

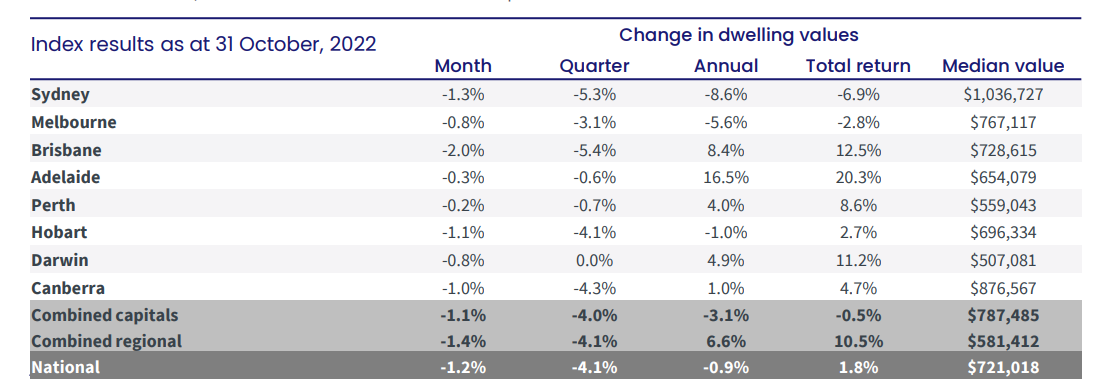

Property

The latest residential monthly property results from CoreLogic show a decline that was not unexpected, with previously rising markets starting to level off (Brisbane, Adelaide).

This said, the number of listings and clearance rates are well down on the same time last year. Quality properties are still moving, though either vendors will need to reset expectations or time on market will continue to drift out.

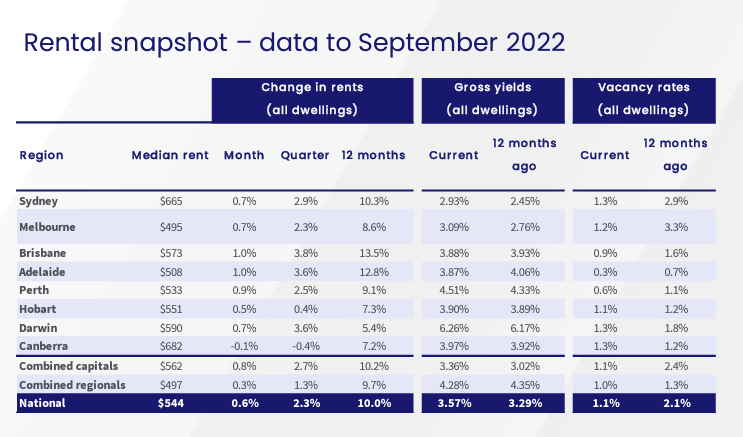

We have been talking a lot about rentals and yields, and the CoreLogic data below shows the anecdotal evidence has fed its way into the official numbers, with the current national gross yield now up to 3.57%.

This is both a combination of rising rents and falling valuations.

Increasing Demand - Migration

A detailed report by property group Charter Keck Cramer shows anticipated Net Overseas Migration ("NOM") will return to pre-Covid levels in 2023. This is coupled with the Federal Government's announcement of an increase to the Permanent Migration Ceiling over the next year from 160,000 to 195,000 people.

Charter Keck Cramer believes that this level of NOM is likely to be sustained and may be at a higher level than forecast. This is also based on data where student and working visa approvals and applications are rapidly increasing over recent months. This will have a material impact on rental demand.

In the commercial office market, data from Barrenjoey showed that vacancy rates in the Sydney and Melbourne CBDs could rise to 15% and 20% respectively, putting city office values at risk. Historically, both markets would work on around a 5% vacancy target. How this manifests into valuation is not totally clear as yet, as there are fundamental changes in how we are working.

Currency

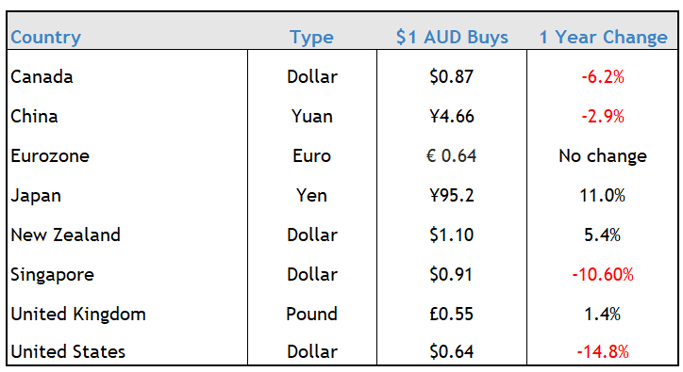

The Australian dollar stayed weak against the USD at around US64¢. It has fallen nearly 15% this cycle, as investors seek safe haven from the prospect of a global recession.

Australia of course is not alone as the table below shows the performance of the Aussie against a basket of other currencies over the past 12 months.

It is a reminder not to look at USD/AUD movements in isolation, especially for those dealing in currency in different countries.

In the past, US dollar appreciation against all currencies is normally the precursor for negative economic growth.

Despite Australia being seen as a relative safe haven, our ties to commodity prices means we tend to get punished in times like these. Relative interest rates also play a role, with rates in comparable markets like New Zealand and Canada at a premium.

Until next time.