%20small.jpg)

Units & Apartments are a critical part of the housing and investment property landscape.

In recent times, their price growth has lagged houses substantially.

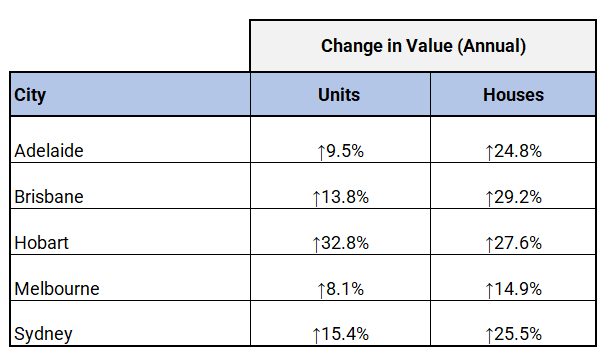

CoreLogic's released Unit Market Update from a little while ago, showed an annual growth rate for units across Australia of 14.3% versus a growth rate for houses of 24.8%.

Advertised unit supply in January 2022 in combined capital cities slowed to -3.7% in 2022 compared to 2021. This is -7.8% below the five-year average.

Hobart is the notable exception, up 32.8% for units compared to 26.3% capital gain for houses.

Although the gap between national house and unit values is at an all-time high, it’s not all bad news for units.

Regional trends tell a different story

Across the board, property growth in regional areas continues to outperform capital cities. The three months from October to December 2021 showed stronger unit growth than housing in Canberra (5.6%), Darwin (2.6%), regional Victoria (5.7%) and regional Tasmania (9.2%). However still well below the five-year average.

Rental demand through 2022

Low vacancy rates will see a continued rise in rentals through 2022. The opening of international borders, the return of international students, and the normalisation of immigration are all contributing factors.

Corelogic data shows that Unit rents are now rising at a faster annual pace than house rents across the combined capital cities and the combined regional areas. We can expect unit and apartment rents to feel upward pressure in CBD areas.

Factors influencing unit price growth

Increasing interest rates will increase repayments, and the rate too for which mortgages are assessed. Therefore, if your mortgage interest rate more like 3-4%, the bank must assess if you can still make repayments if the rate increases to 6-7%. The resulting reduced borrowing capacity may force many to consider more affordable units or apartments.

Investors returning to the unit market, following trends seen in the national housing market.

The push for more high-rise towers in the suburbs, as already seen in Melbourne and Sydney, and not just in previously desired ‘lifestyle’ suburbs.

Increased unit demand in suburban or regional areas as people choose to keep hybrid working habits established during the pandemic, but seek accommodation that offers more space and access to amenities.

Competitive lending offers from non-bank lenders.

Financing Units

Appetite for financing units remains solid. There is a good nexus for what drives lender support for finance, and the factors for which buyers should consider. For example:

- Property Size. Units less than 50sqm may lead to restrictions.

- Location. Some locations have been subject to price variations and hence why credit providers can hold back.

- Development Size. Smaller sizes generally have less strata issues, and they can have a higher land value proportion overall. So more desirable for growth prospects.

- Density. Look for other pending developments in the area. These may drive density and block views for example.

Keeping these factors in mind will therefore mean improved borrowing prospects for financing.

The team at MCP Financial Services has specialised expertise in supporting your business and personal finance requirements.