March 2020 (Rate Decision & Analysis)

For the first meeting of 2020, the RBA left the official cash rate unchanged at 0.75%.

In the end, this was a surprise to markets and it would have been a very close call in the end.

The short term outlook for the economy is obviously a challenging one.

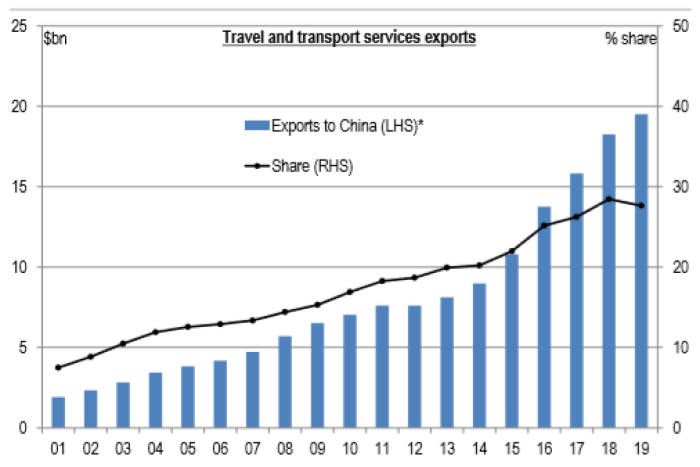

Given our growing reliance on China, Australian GDP is likely to be very soft this quarter (potentially in negative territory) thanks to the bushfires and the coronavirus.

The vulnerability of the Australian economy to China is significant. Exports to China make nearly 10% of Australia’s GDP. This is made up of commodities, tourism and education as we discussed last month.

More broadly, there are macro economic impacts with global conditions very soft, and already trending that way when the Coronavirus hit.

The challenge this time (unlike other virus outbreaks such as SARS) is the ability of Governments to intervene. There is no real capacity for use of monetary policy (with interest rates so low globally) and fiscal policy through spending (with deficits so high) so the recovery we have seen when global events like this occur may not be so swift.

Locally, we may see the Government abandon its budgetary targets and introduce some targeted spending measures to stimulate the economy.

More China fears

More negative short term data from the National Bureau of Statistics, showing factory activity in China contracted at the fastest pace ever in February.

China's official Purchasing Managers' Index (PMI) fell to a record low of 35.7 in February from 50.0 in January, which won't mean a lot to many people other than to state this is significantly worse than during the GFC.

It will certainly start to bite some Australian exporters in particular, and they will need to be aware of conditions in the other countries that they export too as well.

Hasten slowly on more Interest Rate cuts

In the light of calls around the world for central banks to intervene, a sobering reminder of the risk of short term economics.

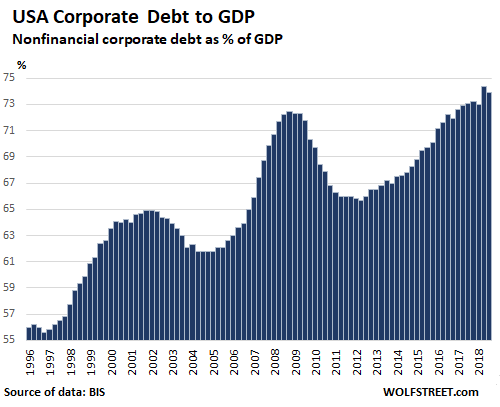

Data from BIS below, shows the growth of US corporate debt to fund spending - ironically a lot of this debt growth has been used to fund share buy-backs and dividends. Whilst that self- confidence is encouraging it does limit the ability of many corporates to absorb financial shocks.

As a comparison, locally in Australia corporate debt is at very similar levels; however it has fallen significantly in recent years, perhaps due to a lack of worthwhile investment projects.

The point of this is complacency. Low interest rates are becoming a generational expectation, so a reminder for business, Government and consumers to consider how they could or would respond if trends eventually reverse.

Money Markets

In the US, some Government bonds dropped to their lowest levels in history this month. This is also being built on the expectation that a strong round of central bank interest rate cuts are imminent.

The same happened on the Australian bond market with all medium term government bonds (up to 5 years) being below the Reserve Bank's cash rate.

[table id=8 /]

The 10 year rate has fallen over 50 basis points since the start of the year, further evidence of expectations of a low interest rate environment for a long time to come.

Short term rates fell too, meaning that the yield curve is trying to hold a normal line.

Property

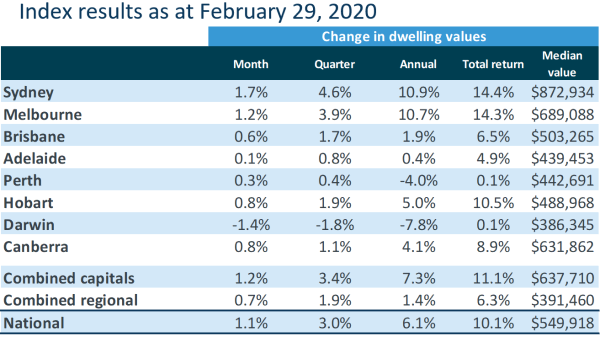

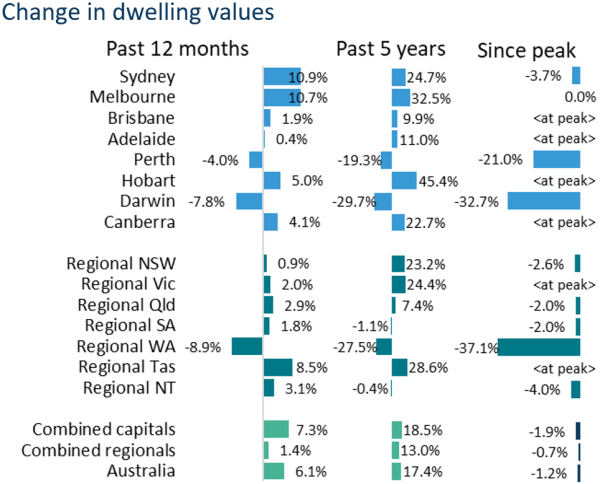

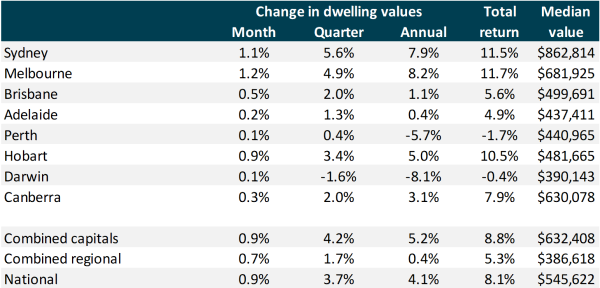

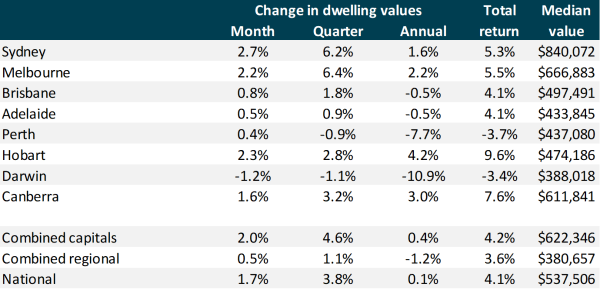

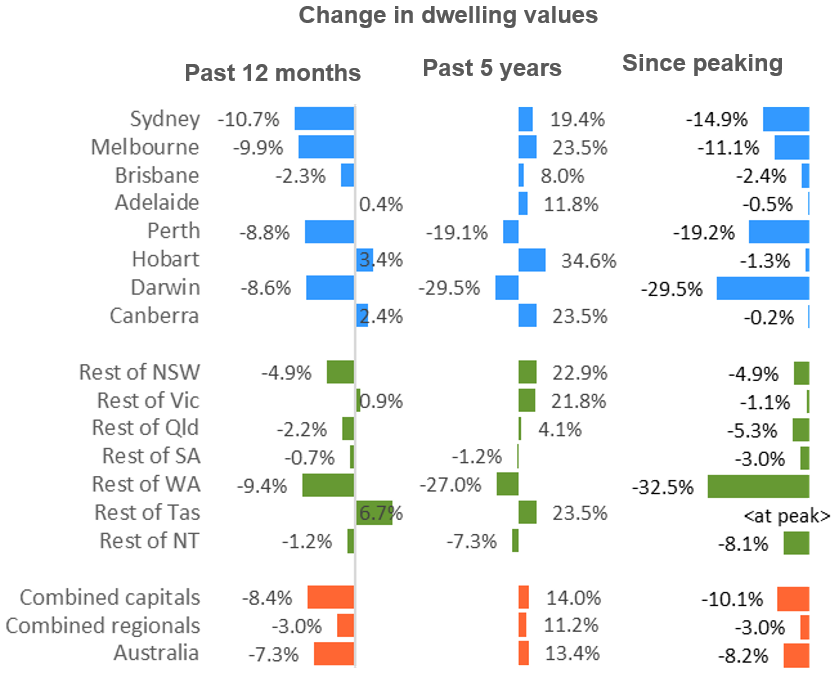

Data from CoreLogic demonstrated the different behaviours when it comes to property and its relative insensitivity to macro economics.

Sydney and Melbourne continued on, the momentum now expanding to other areas including Brisbane, which is growing in its livability reputation.

The growth in Regional areas, by and large has now been outpaced by this capital city growth. Results here though remain diverse between drought affected areas and coastal properties.

As the table below demonstrates, Melbourne has now offically come back from its downturn - clawing back exactly all of the falls of the recent period.

The commercial property outlook is more mixed depending on type and geography. The office market is strong, partly on the back of reduced supply.

Cbus Property's recent approval for a $1 billion office tower in Melbourne’s CBD will be a welcome addition to the market.

Currency

Our dollar has dropped to further lows this month, down below US66c as the market priced in our close association with China.

Again, a weaker dollar is a welcomed development for monetary policy makers, with it easing the need to stimulate the economy through lower interest rates.

-------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------

February 2020 (Rate Decision & Analysis)

For the first meeting of 2020, the RBA left the official cash rate unchanged at 0.75%.

In the end, this is what the market expected though it would have been a close call in the end.

China / Coronavirus

Given our growing reliance on China, Australian GDP is likely to be very soft this quarter (potentially in negative territory) thanks to the bushfires and the coronavirus.

The vulnerability of the Australian economy to China is significant. Exports to China make nearly 10% of Australia’s GDP. This is made up of commodities, tourism and education as we discussed last month.

With the normal flow of overseas students and their spending absent, this will impact the accommodation and related service industries which rely on this flow of activity. Like bush fires, always tough when adverse circumstances are event rather than trend based. Provides no efficient means of utilising the capacity created.

Bush Fires

This may bring policy makers to the rate cutting table faster than otherwise predicted in 2020.

Locally, most economic data analysts can agree that the bush fires are by far Australia’s costliest natural disaster, with tangible costs at the earliest estimate around at least $100 Billion. The tragedy clearly had a role too in very soft Christmas shopping season data which was much weaker this year than previous years.

Business conditions remain very weak. The latest NAB Business Survey showed confidence at its lowest level since 2013, largely driven on the back of weaker profits. So whilst headline employment data was solid enough, there is little or no prospect for any material growth in wages which would be a short term boost to the economy.

Thinking Longer Term - Innovation and Technology

For people bemoaning the devise of our local car industry, and the subsequent lack of transferance to technology and innovation, they won't welcome the release of data from the World Bank's Global Innovation Index.

In short, the data highlighted that Australia’s technology industry is relatively small; and the level of innovation also lags peers and trading partners.

These results are aligned with both NAB & Australian Industry Group surveys showing that business investment into new technologies / R&D was at below average levels. This is again leading the calls for Government to take the lead and stimulate some activity in this area - it is clear big business can't or won't. Or more worryingly they cannot see the return on investment.

Money Markets

Whilst all rates were largely unchanged from the start of December to now, there has been a hub of activity on bond markets driven by the coronavirus.

[table id=8 /]

With the 10 year rate now back under 1.00%, this represents a 40 point drop since the start of 2020.

Short term rates were stable meaning that the yield curve was approaching normal again for a little while, but this fall means it is back to a very flat yield curve.

Property

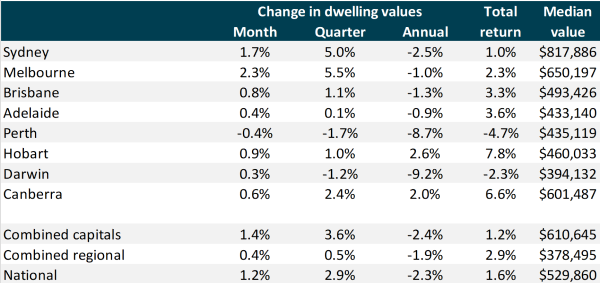

Data from CoreLogic showed the broader recovery in prices is continuing. The momentum which started in Sydney and Melbourne mid 2019, is now expanding to other areas.

This is a very common scenario.

Sydney and Melbourne were 1.1% and 1.2% higher over the month respectively which is a smaller increase than previous months. The next quarter will be an interesting one.

There was also some growth (even a modest amount in Perth) as the table below demonstrates:

As the table below demonstrates, Sydney and Melbourne prices at nearly back toward their peaks in 2017. Whilst Adelaide, Brisbane, Canberra and Hobart are actually at all time highs, albeit with far less volatility over the past 5 years - Hobart aside which at 45% is significant.

Currency

In times of economic uncertainty, markets often flock to "safe haven" currencies and this time is no different. Our dollar has dropped to 10 year lows this month, as the market digested the current issues.

We have outlined previously the very strong nexus between currency and interest rates, with a weaker dollar offsetting any immediate need to take any further stimulus action on the monetary policy front.

For those impacted by a weak Australian dollar we do not see any let up in the short term.

We wish you every financial success in 2020.

-------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------

December 2019 (Rate Decision & Analysis)

For the last meeting of 2019, the RBA left the official cash rate unchanged at 0.75%.

The market is full of mixed signals.

Business conditions for one remain very weak. The latest ABS shows another weak quarter for captial expenditure in particular, which was one of the key areas that the RBA and Federal Government were hoping would lead the charge for growth. Wage growth also remains stagnant, and consumer confidence is low.

On the other hand, the property market has had really strong growth this month (see below) and the Australian Share Market hit highs not seen since the GFC.

With so much conjecture the Christmas break comes at a good time for the RBA, they can wait and see how the market reacts after the recent monetary policy intervention. As a result, we see any further downward movement in rates pushed out deeper into 2020.

The debate about the direction of the economy escalated this month too. With several economic authority cautioning the Government around spending to create stimulus. S&P were ones to state that our precious AAA credit rating could be jeopardised. Whilst they are broadly positive about Australia's prospect for growth, they see that achieving the target surplus should be a priority. Deloitte's published data also broadly echoed this view.

This is the right music for the Federal Government as they sell a cautious approach despite criticism from others.

Growing Household Debt

Of continuing concern to all policy influencers is the growing level of household debt.

The data from ABS/RBA below shows the debt to income ratio of households at record highs. This is despite the record low interest rates, as households struggle with rising essential costs at a time of low wage growth. Compounding this too, is the high asset prices which come partly from the low borrowing costs. To put this in more context, the average size of a mortgage in Australia has increased roughly in line with property prices over the past 20 years. Income growth has not matched this however.

Debt to Income Ratios ("DTI") is a term future generations will become increasingly familiar with, and it is a language of credit assessment being now widely communicated.

Victoria holds the highest DTI at 202%.

Should we be concerned? Yes and No. Household Net Assets positions (from Asset value growth) look stronger than our lower DTI past. The concern remains the exposure to any shocks in the economy, most pointedly to any material changes to the labour market.

This level of household debt is one of the highest in the world.

In that context, DTI can be looked at in conjunction with mortgage arrears rates, which on a national basis are at least not too high by international standards.

The graph below from the RBA does however provide a sobering reminder of the impact of a weak labour market in WA, and the requisite impact on mortgage arrears in that state.

Money Markets

Whilst short term rates were largely unchanged, long term rates dropped over the past month.

[table id=8 /]

With the 10 year rate back to 1.00%, the yield curve flattened again and will be causing concern for the tradional economists.

Lastly, one to leave you with is that around $12 trillion of bonds now have negative yields. By any measure a big number.

Property

Data from CoreLogic showed the highest montly increase since 2003. Sydney and Melbourne were 2.7% and 2.2% higher over the month respectively. Whilst at a national level, values remain around 4% below their peak in 2017, that gap is shortening rapidly.

Whilst Melbourne and Sydney were the star performers the growth was broad as the table below demonstrates.

There were over 3,000 capital city homes taken to auction last week, the largest number since March last year. However, the monthly listings are still well behind last year. It could be that there is a lag between the recent price growth and the willingness of vendors to list.

The demand will likely flow through into 2020 with segements like the First Home Buyers (through the FHLDS scheme) becoming increasingly interested to participate.

Currency

Our dollar reversed this month, as the market digested the impact of the interest rate cut in the US last month, sending the AUD back to "normal levels".

This will have been a pleasing development for the RBA, with a lower dollar offsetting any immediate need to take action on the monetary policy front.

We wish you every financial success as we close the 2019 year.

-------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------

November 2019 (Rate Decision & Analysis)

The RBA met market expectations and left the official cash rate at 0.75%.

This result comes on the back of some recent commentary from Governor Lowe that further reductions to the cash rate should not be assumed. He also stated that the economy could be at "a gentle turning point" of recovery and this is consistent with the "over to you" message for both Business or Government to now drive the economy forward.

It is also a chance for the RBA to sit back a little and wait to see how the market reacts after this busy period of monetary policy intervention.

There are some short term results too that may put a pause on the easing button.

The inflation result for the September quarter was above expectation (1.7% annualised) even though still below the RBA target range of 2-3% and employment levels improved slightly. The upward momentum in property prices is also a contributor as we discuss below.

The Government has also been active in trying to create an environment where the banks are able to make credit more readily available. This includes both First Home Buyers (through the FHLDS scheme) and the SME sector (via a welcome clarification of the definition of consumer credit). As Governor Lowe states, "lenders should not be so scared of making a loan that goes bad that they don't provide the credit the economy needs". Some welcome common sense.

Money Markets

In support of the stabilising rate story, long term rates etched up a little over the past month. The market is no longer fully pricing in the prospect of another rate cut in the short term.

[table id=8 /]

With the 10 year rate at least now above 1.00%, the yield curve is a little more encouraging and provides a little more support for the economy in the longer term.

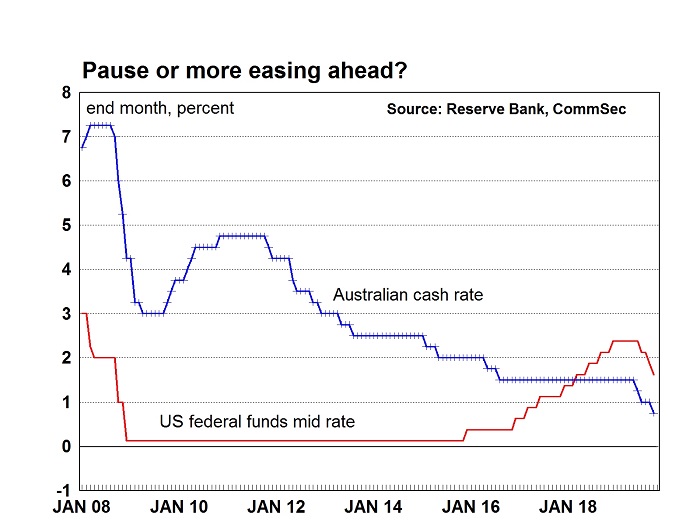

Perhaps of more concern to the RBA this month was the US Fed's decision to drop its central interest rates by 25 points. As the RBA/CommSec graph below demonstrates, we have got ourselves into a bind where we do not want exposure to anything that accelerates demand for our currency.

As we discuss in Currency below, the impact of global interest rates are very significant.

Property

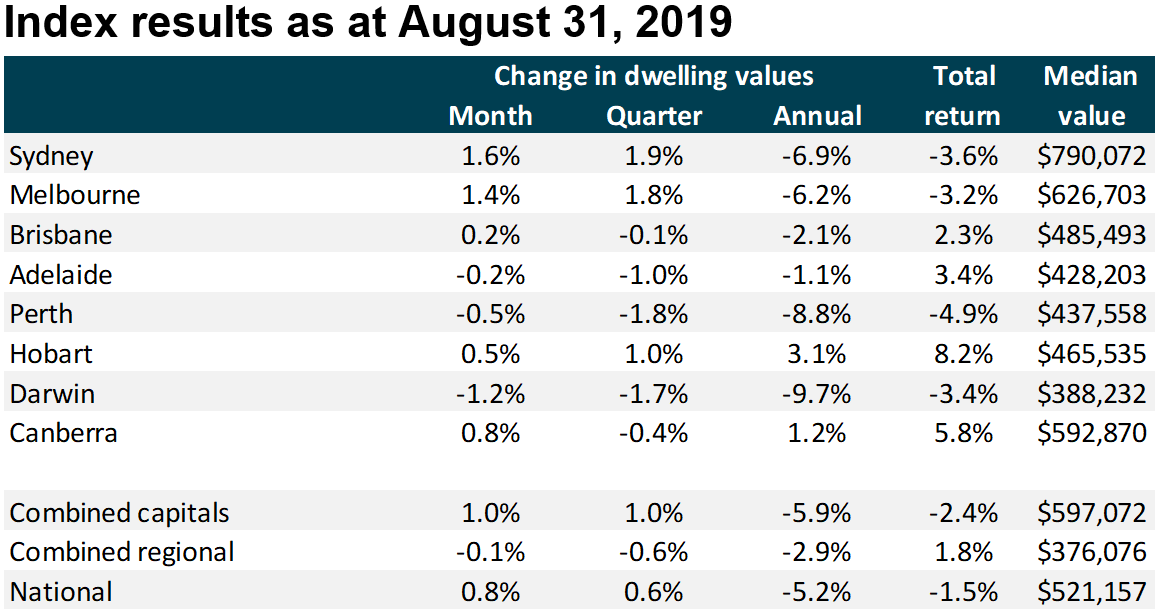

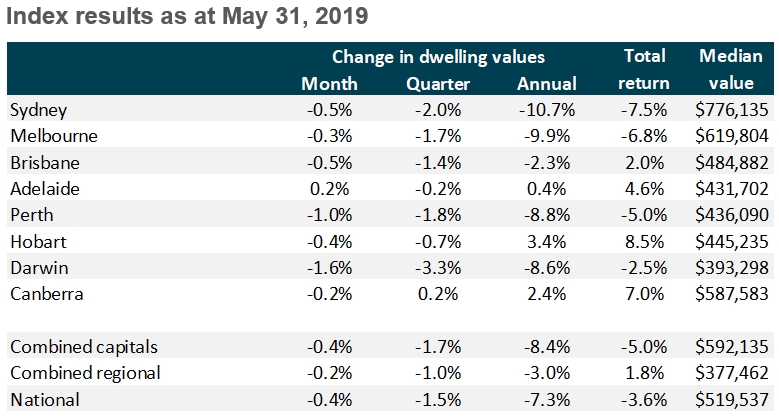

The Residential Property market remains strong, as data from CoreLogic shows, confirming a 1.2% rise in national dwelling values over the month. The October result was the largest month-on-month gain in this index since May 2015, and provides more evidence that the levels at June 2019 may have been the bottom of some markets.

Melbourne, followed by Sydney were the star performers.

One of the reasons for this spike is the First Home Buyer market. They comprised almost 30% of the national market for owner occupier home loans; well above the decade average of 25% according to ABS data.

This can be explained by a combination of factors including housing affordability, lower interest rates, more favourable home loan servicing rules and State Government incentives.

On the commercial property front, Sydney and Melbourne continue to be the best performing markets, though both not growing at the pace of recent years. This said, yields cannot drop too much lower so capital growth will need to come on the back of increased rents.

Currency

Our dollar rallied on the back of the interest rate cut in the US. A reminder of Chairman Lowe's comments last month which demonstrates the challenge of managing all competing economic variables.

"If we were to maintain our interest rate in the face of a decline in the global rate, our exchange rate would appreciate, likely moving us away from our goals for inflation and unemployment. So we have to move too and this has been a consideration in our recent thinking on interest rates".

Accordingly, as US interest rates fall, Australian savings accounts become more attractive thus creating a demand for our currency.

This is not sweet music for the modern economy.

-------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------

October 2019 (Rate Decision & Analysis)

The RBA met market expectations and cut the official cash rate by 0.25% at its meeting this month to 0.75%.

The economic outlook remains pretty dour, with events both worldwide and locally causing concern. The same issues remain - little or no real wage growth, a shrinking residential construction cycle, benign business sentiment, etc.

Last month, we discussed a slowing economy and this is reflected in a GDP trending at 1.4%, well below all targets and expectations.

The discussion is becoming increasingly political; the RBA has not got much more room to move in its efforts to drive the economy, so one expectation is that Government will need to take the lead. Said former Treasurer Peter Costello "Another 25 basis points frankly isn't going to do much to stimulate the economy". The record low interest rates are also driving concern about a rebounding property market, and any resultant growth in household debt.

The Government is still looking to business to take the lead, and to invest. Businesses are saying that despite the low cost of debt or equity, the opportunities to invest are not attractive enough at present.

So, many commentators are screaming for the Government to stimulate the economy through spending.

This is further exacerbated by falling consumer confidence as shown by the ANZ-Roy Morgan Research data below which is really on the back of nothing specifically.

In this context, hard to know who should go first.

Money Markets

Locally, bond rates stabilised this month. With the market pricing in the prospect of a rate cut, short term rates fell a little.

[table id=8 /]

So as a result, although all long term rates are under 1.00%, the yield curve looks a little more normal. However, the money market remains in uncharted space. We are now in a world where Bonds don't actually yield a return. Rather, they are a home for speculators that trade in Bonds ignoring the underlying yield in the hope they can be held and sold for more. At some point that must be fool's gold.

Over the last week, there have also been some real structural concerns for the financial world. Without going in to all the detail, we had a short term liquidity crisis with the U.S. Federal Reserve having to step in and support the market. Watch this space.

Property

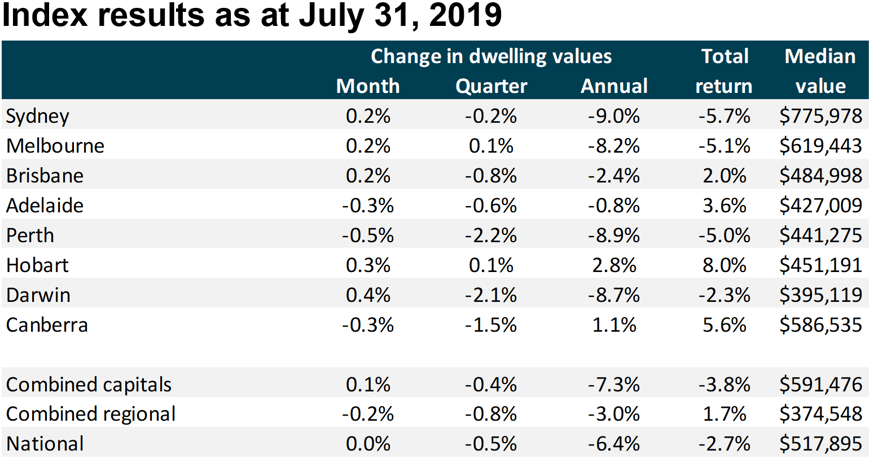

The Residential Property market remains strong, though as data from CoreLogic shows, this is off the back of much lower turnover levels.

The momentum is turning slowly as prices improve, but it is relevant to follow through the consequences to the economy of the low level of turnover.

CoreLogic's Tim Lawless makes some timely reminders about what reduced property turnover actually means. "Reduced housing activity implies less spending on retail items such as home furnishings, white goods and appliances. With both values and volumes falling, there has been a hit to state government stamp duty revenues and of course we see real estate industry and finance sector participants receiving less income based on lower rates of sale and lower values."

Timely comments in the context of the soft economic data above.

Currency

Our dollar continues to be soft but more stable over the last month. If ever you doubted the strong relationship between interest rates and our currency, Chairman Lowe put that to rest with his comments this month as below:

"If we were to maintain our interest rate in the face of a decline in the global rate, our exchange rate would appreciate, likely moving us away from our goals for inflation and unemployment. So we have to move too and this has been a consideration in our recent thinking on interest rates".

Maintaining a low exchange rate, despite any longer term implications, seems a priority for the "now" economists.

-------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------

September 2019 (Rate Decision & Analysis)

The RBA left the rates unchanged today.

The theme here is increasingly dour with events both worldwide and locally causing concern. A soft quarter of data means a forecast annual growth rate of only 1.5%, the lowest in ten years. This is coupled with the largest fall in residential construction rates for almost 20 years.

Despite the record low interest rates, businesses here and globally are not confident about capital investment and this is where the increasingly public debate between the RBA and the Federal Government remains hot.

On one hand, the RBA is making clear that monetary policy (with its record low rate settings) has done all it can to drive the economy, and it is saying the Government needs to take the lead and drive investment. "Monetary policy cannot deliver medium-term growth" said Chairman Lowe.

The Government, especially in a fragile global economic environment, is determined to get the budget back to surplus and keep something up its sleeve should things deteriorate further. In turn, they are urging corporate Australia to stop returning excess capital in the form of special dividend and buy-backs, and to invest to get the economy moving. Probably a tough ask in the current environment of uncertainty but like the RBA, they have to put their case on the agenda.

In terms of who is right, depends on your outlook. In the short term, the RBA is concerned about the short and medium term and the ability to create employment, keep inflation within its target, and indirectly manage our exchange rates. The Government, is also concerned about already spiked assets prices and high household debt (i.e. what if we eventually return to a more normal interest rate environment?). More the point, they stress that spending on infrastructure or other stimulus needs to be well considered and yield a return in the long term.

At an altruistic level, we also need a consistent set of principles. We urge households to live within their means and we criticise everyone but ourselves when we don't, so perhaps Government needs to ensure that any stimulus spending is responsible to set the right tone. There is also more to infrastructure investment than money, you also need to be able to mobilise the other resources (e.g. labour) to deliver them efficiently.

The discussion has remained around given the recent cuts a chance to work, and we are at least seeing that in the property market to a degree. This said, with money markets where they are presently, further cuts are still expected before the end of the year.

A shout out too to our neighbours in New Zealand where they recently cut their cash rates by 0.50% (50 basis points) to 1.00%. The 50 was a shock to the market. I always think staggers of the smaller 25 point cuts are "death by a thousand cuts" and are largely immaterial in the minds of the people you are trying to impact. 50 makes more of a statement and more likely to change behaviour.

Money Markets

We head to unprecedented levels for market interest rates as we show below. Rates took a big dive over the last month prompting the traditional economists to point to a global recession ahead.

All long term rates, including 10 Year Bonds, are all under 1.00% with the yield curve now heavily inverted. The US yield curve officially inverted between 2 and 10 year maturities – i.e. you get less on 10 year yields than a shorter 2 year maturity.

Given our place in a global economy, the RBA raised concerns that rates may need to continue to fall. Overseas, the Eurozone is approaching a structural crisis. Take Denmark, where they have had central rates below zero since 2012.

The traditional model of deposit funding being cheaper than market funding has been turned on its head, meaning that banks may need to start charging for deposits or find other ways to make money.

More broadly, the view in Europe is that these interest rate conditions could be with us for years. The German 10 year bond yields have fallen by over 65 basis points this year into negative territory, amid inflationary concerns.

To round out the story, Germany have issued a 0% coupon 30-year bond at a yield of -0.11%. These 30 year yields rates now mean all rates in their market are now in the negative, as the chart from FIIG Securities below demonstrates.

The yield curve is in uncharted space. In fact, with these negative rates the Government is being paid to borrow.

Property

The Residential Property sentiment continues a positive story. Anecdotally, the talk and feedback from Agents is that vendors expectations are meeting market. At this new level, competition is intensifying especially in the Melbourne and Sydney markets.

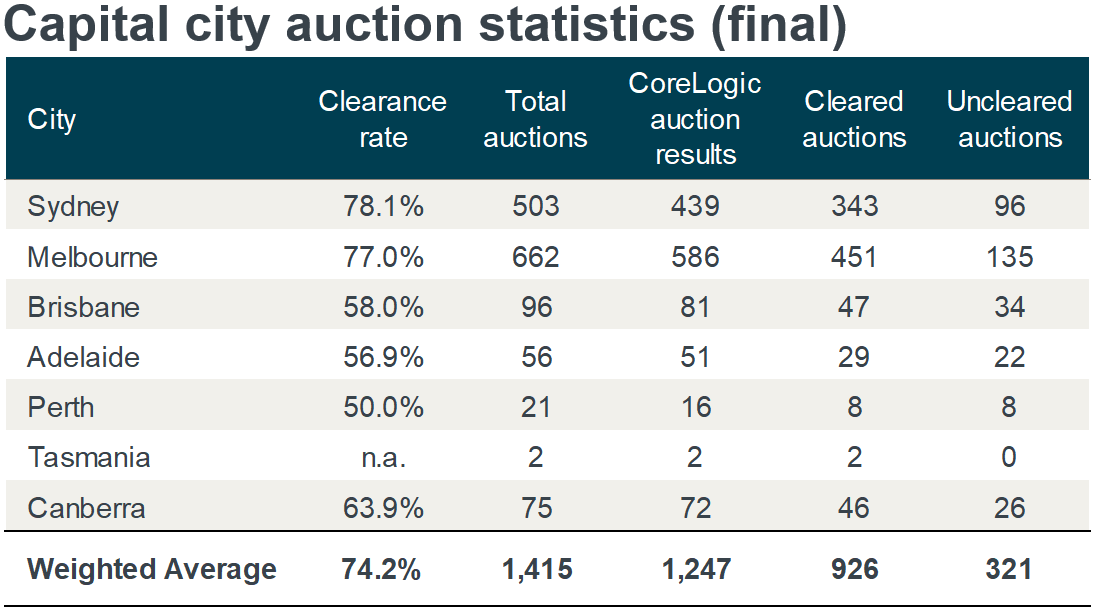

As the data from CoreLogic below shows us, Sydney and Melbourne clearance rates are leading the way.

So that's the lead data, the lag data is confirming the market improvements as the CoreLogic table shows below:

Currency

Our dollar continues to be weak. With Australia's reliance on a China economy that is slowing, combined with the US/China trade war, is combining with other factors to drive a lower Australian Dollar.

We talked about the fact that there are always winners and losers from a weaker dollar. We seeing it at the petrol pump, with our reliance on the U.S. sources driving up price increases. This is flowing into other Australian businesses that rely on imports that contribute to their product offerings.

-------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------

August 2019 (Rate Decision & Analysis)

The RBA dropped Official Cash Rates by 0.25% to 0.75% at its meeting today.

Over the course of the last week, markets have been pricing in the prospect of the cut to an even money bet. So the broader RBA comments will be interesting this month with the easing bias approaching its low point.

The discussion had been around given the recent two cuts a chance to work. In that context it was interesting to see that RBA Governor Lowe forecast that we should "expect an extended period of low interest rates". The focus remains too on the level of inflation, we can expect another cut in the future if inflation targets in the 2-3% range are not achieved.

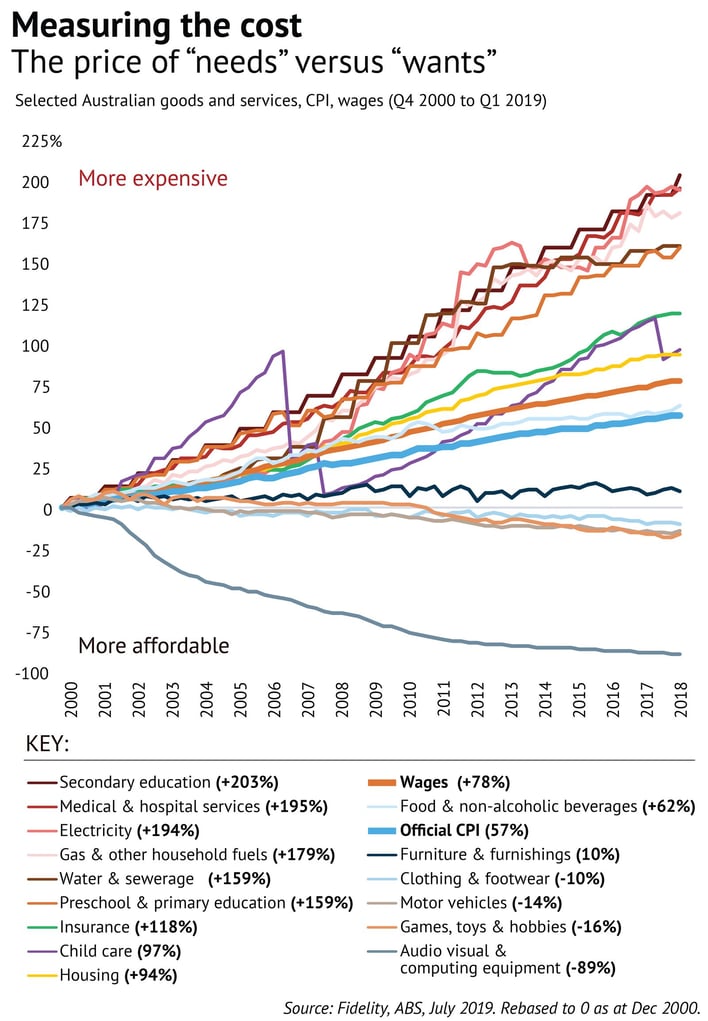

The Inflation Story

With the RBA focus on inflation, recent data from the ABS and analysis by Fidelity International was interesting. Their investigation tracked price movements in sub-categories in the consumer price index ("CPI") since 2000 as shown below:

Official CPI has gone up 57 per cent in this near 20 year period. In the context of the RBA's wants, on an average basis it is within its specified target range.

The challenge is the allocation of prices, or "needs" and wants" as Fidelity International puts it. Most of the need items have increased well above CPI - secondary & tertiary education, healthcare, childcare etc. This has obviously put huge pressure on households, as whilst wage growth has exceeded CPI over the same period, there is a greater concentration of spending to the expensive needs categories.

This in part explains the challenge for our retail economy, with consumers looking to access "wants" cheaper and more efficiently that before. Organisations or Governments that replicate innovation that drives more cost effective "needs" accessibility will be the winners in the long term.

In part too, this explains that despite the record low interest rates, we are seeing mortgage arrears trend up slightly as well.

Last month, we discussed the stakeholders urging the use of cheap debt to fund large infrastructure programs. This month, the ratings agencies bit back and highlighted the need for balance. S&P Global Ratings is one that has urged the Federal Government to maintain its AAA credit rating. Whilst acknowledging that this would be at the expense of injecting fiscal stimulus into the economy.

We talked about the political challenge for Federal Government, with the promise of returning the Budget to surplus. However, with monetary policy easing no longer a material option, an economic shock or two will test that resolve.

A key success factor for Government to get return on investment whilst at the same time giving the stimulus that the economy will need. Spending for the sake of fuelling the economy in the short term (remember the $40 Billion largely wasted on Schools and Recreation post GFC?) won't cut it.

The country needs it best minds on any fiscal stimulus, with infrastructure spending that yields a return at its heart. Hopefully the politics can take a back seat in this regard.

Money Markets

Another new low for market rates as we show below.

[table id=10 /]

The bench-marked and traded 3 Year Swap Rate now well below 1.00%, with the 5 year heading that way too.

What does this all mean? Judging by markets they have taken on Governor Lowe's comments. The current Swap rates indicate that the cash rate will sit not higher than 1.0% over the next 5 years.

This is more evidence that this yield environment is generational. When the next tightening cycle eventually starts again, there will be have to lots of warnings about the "tough old days" of 5 or 6%. Sorry Baby Boomers, your old stories of 17% will be well and truly archived.

Against this weak stories of the economy, the ANZ-Roy Morgan Consumer Confidence Index remains up over its long term average. More evidence again that the interest rate story is also a global one.

Property

The Property sentiment continues its optimistic outlook. Melbourne alone had a great last weekend, with a clearance rate at over 75% albeit from smaller volumes.

As the data from CoreLogic below shows us, Sydney and Melbourne are back in positive territory over the past two months. The 0.2% lift in Brisbane was the first consecutive rise since November last year too and there is some momentum there. Anecdotally, there is interest in a range of property categories as yields in other asset categories continue to dwindle.

Perhaps the lag trend to Regional areas is softening too.

As the CoreLogic data shows further below, it will be interesting to follow values whether the improvement is sustained. In rolling the data forward, an improvement will show up in the 12 month changes which should start to diverge away from the "since peak" results.

Currency

After a stable period, Australia's currency fell against the U.S. Dollar. This was in part driven by the RBA's focus on low interest rates. At some point, the fundamentals said that it will have to have a material impact on our dollar.

Right now, we are at levels not seen since the GFC. For those in the market wanting favourable currency conditions, now is your time to shine. Conversely, there are always losers and higher input costs from a weaker dollar might find its way into some price increases.

-------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------

July 2019 (Rate Decision & Analysis)

Despite strong market expectations, the RBA left official Cash rates at 1.25% at its meeting today.

Markets had been pricing in the strong prospect of the cut to another record low. This still looks firmly on the agenda.

The headline discussion has remained around local issues, such as progress in reducing unemployment and progress towards growth and the inflation targets. However, global influences are dominating the thinking right now.

Our exchange rate is one, with the RBA wanting to avoid any upward pressure on our dollar. This is especially challenging with most central banks easing interest rates worldwide. In other words, you don't get the bang for your buck in terms of stimulus when competing with other countries too.

As RBA Governor Dr Lowe reminds us, "we trade with each other, not Mars".

One of the beneficiaries of these low rates is Government, with States going into debt to fund large infrastructure programs. The RBA in fact has been very vocal in the opportunity to take advantage of cheap rates to fund infrastructure projects, adding that monetary policy is losing its bite (no surprises there).

This may however be a political challenge for Federal Government, balance cheap money with the promise of returning the Budget to surplus.

There was a flurry of activity with lenders after last month's cut, and some have already played their hand with balancing out their fixed and variable interest rate offers.

These low cash rates put pressure on bank margins, they will need to balance the political pressure and their need to protect profits which have been sliding over the last year.

Money Markets

If I said last month rates were low it certainly wasn't the bottom as we show below.

[table id=7 /]

In an era of surprises, we even saw the commonly bench-marked and traded 3 Year Swap Rate below 1.00%.

Australia is obviously not alone in terms of money markets with bond yields collapsing across all established markets. This of course has many economists concerned about what lies ahead, especially with growth slowing in China.

There are however more signs that this yield environment is approaching generational proportions. Take a strong economy such as Austria. Following demand from a few years ago, they have just released a 100 year bond with a fixed coupon of 1.10%! For many investors, this at least provides certainty especially if you compare this to Germany's -0.25% return on a 10 year bond.

In terms of spending on infrastructure, State Governments in Australia could look to China. The graph below (Courtesy RBA) shows that their local government bond market has grown rapidly, overtaking the US in recent years. It is now the largest municipal bond market in the world.

The central Government is still strongly supporting this program, though there are signs that the infrastructure pipeline could be slowing down. This is what builds uncertainty to China's partners around the world.

Currency

Australia's currency is still soft against the U.S. Dollar, but stabilising. It is down just over 5% over the last year. This was probably less than I had expected, especially given the historic position of our interest rates - well below the U.S.

Strong commodity prices and our narrow current account deficit have offset the imbalance in interest rates, and with the Fed's next move likely to be down, this could put some upward momentum into our dollar. As always with currency positioning, this suits some and not others.

Property

The Property sentiment remains cautiously optimistic.

Clearance rates are not always the most relative statistic, though they are a barometer of activity and the CoreLogic data continues to show an improvement.

Again, anecdotally, we have seen more demand and stronger results in many instances for vendors.

-------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------

June 2019 (Rate Decision & Analysis)

The discussion has been centred around muted growth, and business investment, household consumption and inflation numbers. More broadly, as we outline in Money Markets below, the official cash rate is now more relevant as market interest rates have already fallen down around them in anticipation.

The momentum to drop was offset by a post election burst in positive energy. This was reflected in a stronger share market and broader sentiment generally, this may not be explicit in the minutes but no doubt had a bearing on this result. The APRA decision to review its prescribed lending activity for mortgage lending would have also made an impact too, along with the pending tax cuts.

Now the fun begins as we see how banks will react as they, like the market, had expected a drop. Mortgage holders may have to temper their expectations, as we do not expect that lenders will continue their aggressive pricing.

Money Markets

The yield curve in Australia was technically inverted as the table shows. However, we have had to create history to drive that - with the 180 Day Market Rate at it lowest ever point in recorded history.

[table id=7 /]

It did get me looking at the history books which took me to a time in 1974 when the short term was actually over 21%.

The current rates are almost unimaginable if you, like me, studied any traditional economic theory. If a futurist had told me we would have rates at this level in 2019, I would have imagined an unprecedented level of economic carnage.

One of the considerations to hold rates was having some room to move in the future. As a risk to our economy moving forward is that we do not have the lever of monetary policy. This was a fear always shared by the traditional economists and there has been a chorus of support from many business leaders too.

We are at an interesting in the financial cycle. The graph below (Courtesy ANZ) shows the gap between the Cash Rate and the 10 Year Bond Rate over the last 30 years. The 10 Year Bond is now at the lowest level in history. Traditionally, this would suggest that the outlook for the economy is negative.

There is certainly precedent for this as we look back in history, though I am not convinced this time. The paradigm for interest rate policy is different worldwide, with central banks much more proactive in using monetary policy as a tool to manage economic health.

We must also consider the debt bubble fear, with many countries feeling that they cannot increase interest rates at present regardless of the other economic variables..

Currency

A big reason that gives the RBA to lead such low rates is the relative health of the Australian dollar. The dollar's strength is supported by the robust commodity prices and our rapidly falling current account deficit. This narrow deficit means that we are less exposed to the traditional currency weakness that is associated with low interest rates.

In other words, we are almost able to fund ourselves.

Property

Property is out of the political spotlight (amazing how fast we move on) and anecdotally the sentiment is up. The last month's worth of data below obviously include pre-election figures - so the following month will provide some insights.

A guide of post election activity is via the latest auction clearance rates. The last week saw Melbourne continue to be above 60%, whilst Sydney clearance rates broke the 60% mark for the first time in a long time.

The updated Corelogic data shows a slowing correction.

With some early signs of confidence returning - it is timely to look at more Corelogic data to put a marker of longer term trends.

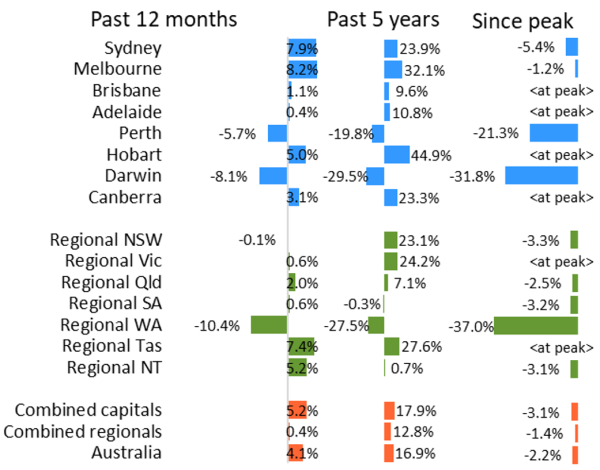

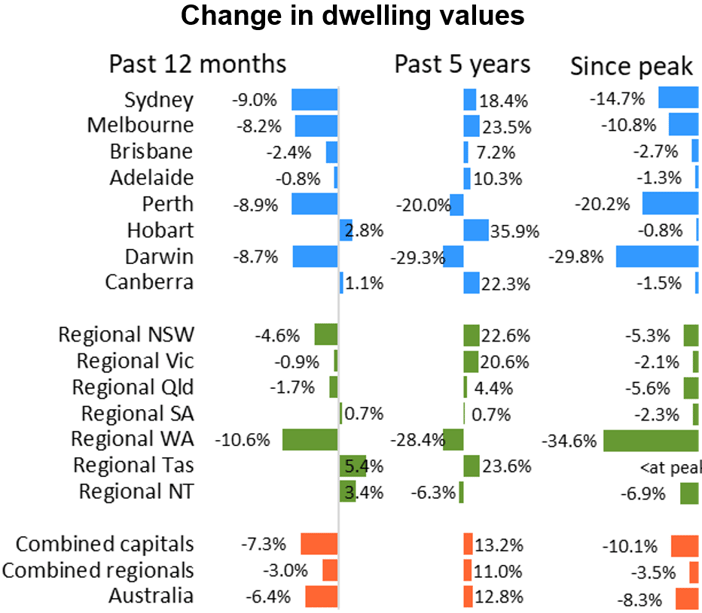

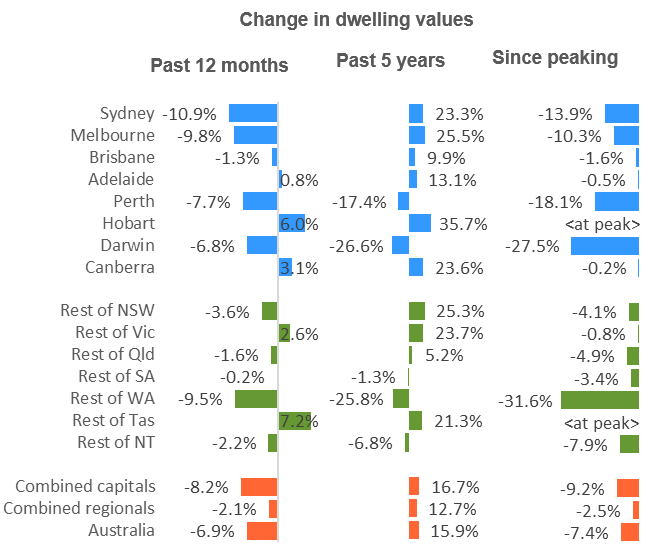

Dwelling values have fallen by 8.2% from their peak, and the stark results in Perth, Darwin and parts of Regional Queensland are important reminders that property can be volatile.

We have commented previously about the lag rise in many Regional areas, but it is also worth reflecting that over a five (5) year period they haven't out-performed capital cities.

The next three months of so of data across the entire economy will be worth a look.

-------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------

May 2019 (Rate Decision & Analysis)

The RBA left interest rates unchanged at its meeting today.

In the end this was a surprise to many, with the market pricing in the strong prospect of the a 0.25% (25 basis points) cut to the official cash rate.

The discussion has been centred around muted growth and inflation numbers. More broadly, as we outline in Money Markets below, there is a growing call that the official cash rate is becoming less relevant as market interest rates falls around them.

At least it maintains something up our sleeve should we really need it.

Money Markets

Well, the yield curve in Australia is not yet inverted (i.e there is still a gap between short and long term interest rates) as the table shows. However, we have had to create history to maintain that - with the 180 Day Market Rate at it lowest ever point in recorded history.

It did get me looking at the history books which took me to a time in 1974 when the short term was actually over 21%.

[table id=7 /]

We talked last month about concerns around the levels of global debt. There is no doubt that Governments and households are generally under pressure and that is why it is hard to mount a case for increasing rates in the medium term.

As these falling interest rates have sustained, we have seen this reflected in falling fixed interest rates for borrowers. We have seen some competitive fixed interest rate offers in the market currently for both consumers and businesses. Might be a brave strategy to fix now but the bottom perhaps isn't too far off.

Property

Property is firmly in the spotlight - especially given the current political debate around the proposed ALP changes to negative gearing. Despite some of the sensationalist campaigning from all sides of politics, the positive is that a discussion has started on a range of housing and the issues that relate to it.

The discussion expands to demography, including infrastructure and immigration, with some of the content bringing in some longer term thinking. What is clear is that there is no perfect solution. On one hand we are concerned about falling property prices and the need for strong personal balance sheets, on the other we want housing to be accessible and affordable.

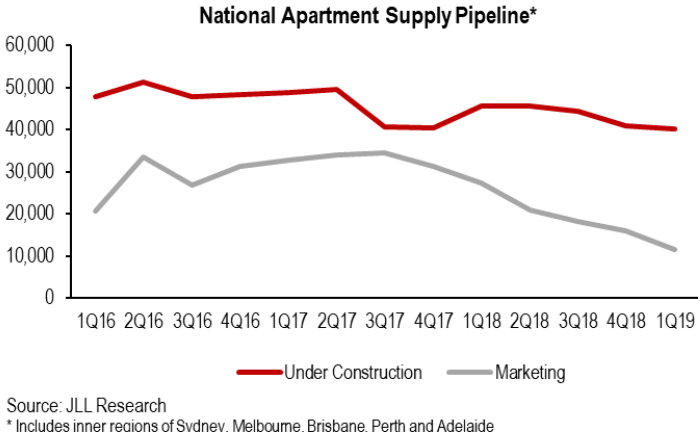

With this in mind it is timely to look at some research data from JLL specifically in this example around apartments.

This is always one of the most tricky assets.

JLL data shows that number of apartments under construction across Australia has dropped by approximately 10% over the past year, and more interestingly, the number being marketed has fallen by nearly 50% as below.

When we go in the detail by major cities, you can see the lead and lag affect of negative sentiment. Brisbane leads the stats (36% reduction in Construction, 59% in Marketed) and if you recall the sentiment has been very weak even before the current overall cycle downturn. Sydney comes in next (24% Construction, 77% Marketed)

Melbourne’s construction level is actually up 15%, though the lead indicator of marketed has fallen by 51%.

According to JLL (and well seen in our connections too) projects have been reallocated redesigned for other uses including offices, hotels and student accommodation amongst other things.

Whilst this data may not be surprising, a note of caution is that our population continues to grow strongly. If these trends continue we could see some supply pressures down the road.

The sooner the election comes and goes, whatever the outcome, the better.

----------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------

April 2019 (Rate Decision & Analysis)

The RBA left interest rates unchanged at its meeting today.

Much of the macro economic data - including employment and stronger than expected commodity prices - is solid enough though business and consumer confident is muted.

According to ABS data, the unemployment rate dipped to 4.9% in seasonally adjusted terms which is it lowest rate since 2011. This is a little misleading, with the participation rate down and wage growth very stagnant. We see this as a key driver of interest rate pressure at a local level and increasingly it is seen as underpinning our economy. This is despite any growth in wages or indeed the small business profits to fund them.

The real story is interest and bond rates as they fell sharply, particularly with the 10 year bond rate falling to a historic low. This is part of the growing fear around the global economy and slowing growth. This was also further fuelled by the US Fed's comments around a lack of expectation of further rate increases in 2019.

Money Markets

We have talked previously about an inverted yield curve - the US at that point now and Australia is marching closer. The "spread" between the Aussie 180 Day and 10 Year Rates is now non-existent where the historical average is around 0.75%.

[table id=7 /]

As the table shows, sentiment is very weak, and many economic commentators are pricing in a possible cut in interest rates this year.

One of the biggest fears worldwide is the level of global debt. This in part explains why we have negative nominal yields in many parts of Europe and Asia and why it is so hard to increase interest rates. So what is a negative yield? In simple terms it involves a loss of your capital invested. So if you make a bank deposit or buy a financial instrument, you receive at maturity an amount less than the original investment undertaken.

So if economic conditions are to deteriorate it is more reason why the RBA has to hold tight as long as possible.

If these falling interest rates sustain, funding cost pressures on banks should ease over the coming months which could be good news for business or mortgage holders. Typically, fixed interest rates see the immediate benefit of easing costs which explains some of the competitive fixed interest rate offers in the market currently.

Property

It has been another headline month for Property, especially dwellings.

CoreLogic data showed another 0.6% drop in March. Though this was actually the smallest of the month-on-month decline since October last year. While there are still more downside risks to property, anecdotally from our dealings with property transactions, perhaps it is finding a level.

To provide a broader perspective, CoreLogic also extended out their research data over the last 5 years which makes for a more balanced approach to the current scenario.

Despite the current weakness, the national index remains 15.9% higher than five years ago (This includes around 25% for both Melbourne & Sydney). Again, we need to continue to look at different parts of the country where results in Perth & Darwin are impacted the most materially.

It also puts the Regional story into more context as growth still remain below capital cities over this sustained period.

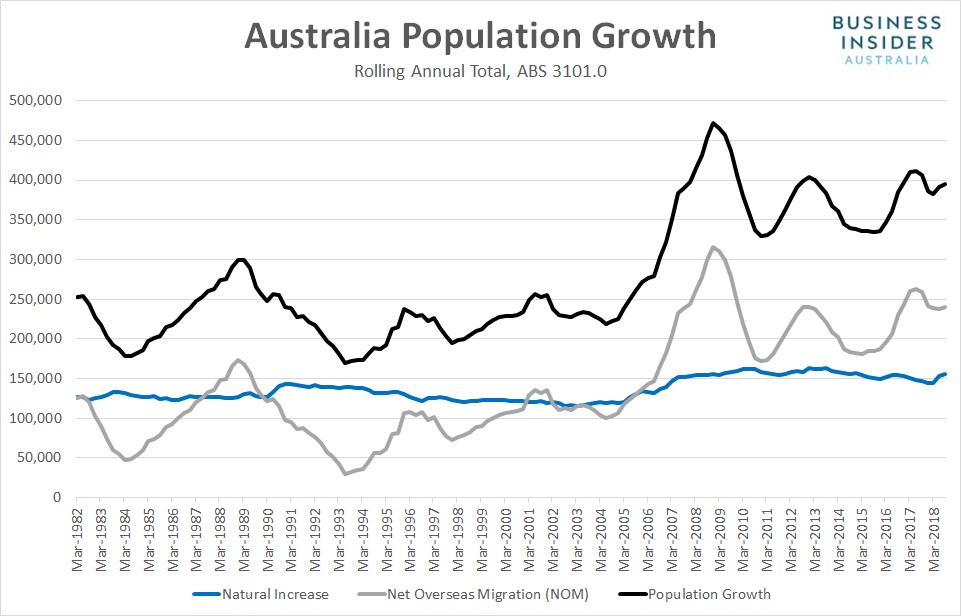

As further analysis, much has been said about the impact of Australia's Population growth and its impact on infrastructure, employment and of course property prices. Data from the ABS and the Business Insider Australia below is interesting.

Australia’s population grew by nearly 400,000 in the 12 months to September 2018. Overseas migration drove the majority of the increase, lifting by 240,000 whilst the natural increase was around 155,000.

In terms of the impact on property demand in the medium term, nearly-three quarters of new arrivals settled in New South Wales and Victoria.

It is an understatement to say that Property will remain firmly in the spotlight as an election issue; however, the issue of population growth and the congestion that it brings is gathering significantly more commentary lately. This issue, and the responses by policy makers, will make the long term property story even more complicated.

----------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------

March 2019 (Rate Decision & Analysis)

Official interest rates remain unchanged at 1.50% from the RBA monthly meeting held today.

The softening economic mood continues, with Australia’s economy slowing sharply through the second half of 2018 accordingly to GDP data with more results expected later this week. Consumer confidence is also relatively weak, despite a rebound in recent weeks. Some offsetting news is the robust employment data, along with positive business sentiment which is giving confidence to the RBA that current monetary policy settings are appropriate.

Soft data is not a total surprise, with a lot of tensions (both economic and politically) and a looming Federal Election to be announced in the coming weeks.

Globally, economic momentum has slowed across Europe and China, though an upswing in the U.S shown in their latest GDP data.

Locally, credit growth has been at its lowest levels since the early 1980's. This is perhaps not a surprise to many. This data is being lagged by the difficulty in refinancing and the number of interest only loans transitioning over to a principal & interest basis of repayment.

Money Markets

On the money markets, short term and long term rates are both weaker. The "spread" between the 180 Day and 10 Year rate remains at around 20 points.

[table id=7 /]

As the money markets show below, sentiment remains weak, and the direction of interest rates remains uncertain, despite the market pricing in a possible cut in interest rates this year. Funding pressures also continue to grow with more out of cycle interest rate rises on mortgages. Without being too repetitive, we can only hope that the RBA keeps something up its sleeve should economic conditions deteriorate more than expected.

Currency & Property

The AUD has been surprisingly robust again. Robust commodity prices remain a supporter for the Australian economy despite the other soft data.

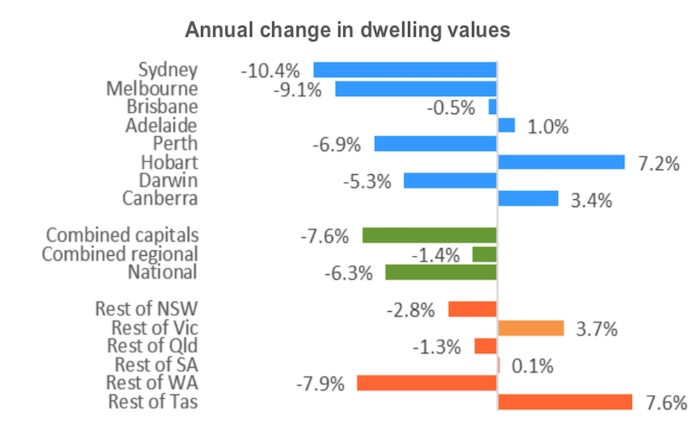

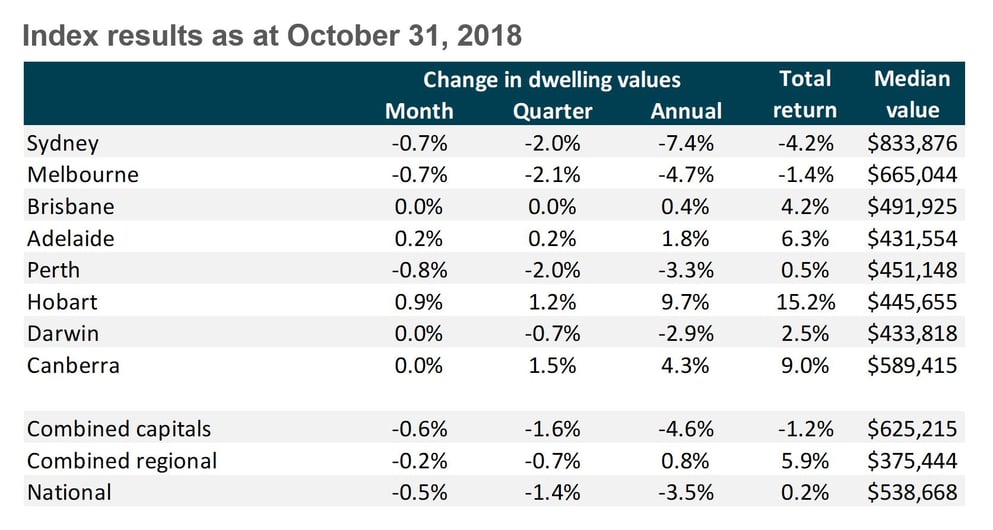

Aligned to the low credit growth above, Property continues to be weak. In fact, there have been 16 consecutive months of falls on a consolidated basis.

CoreLogic data below shows Sydney & Melbourne in particular continue to decline, though at a slower rate. Auction clearance rates, particularly in Sydney have improved a little as well. Perth looks like it may be turning the corner.

This all said, anecdotally things still feel weak. Presently, vendors are not testing the market in any real volumes and that will not happen whilst employment remains robust. Poorer quality stock in particular is not getting any interest and the buyers (foreign and otherwise) that were active in the market previously are absent.

Most experts predict there is a little more to come.

Results are very divergent across different markets as the table above shows. We expect that this will even out as the year goes on.

-------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------

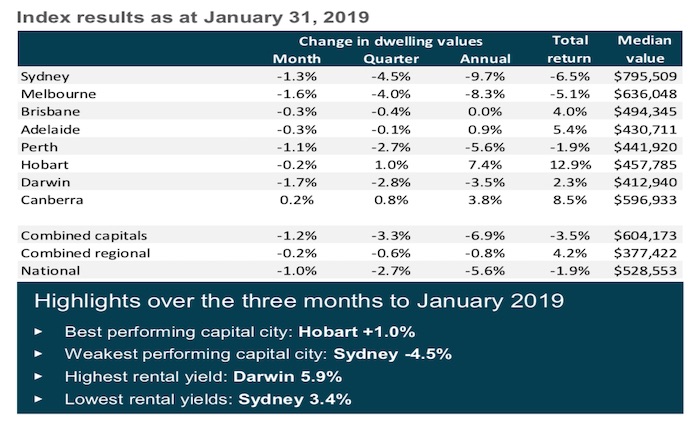

February 2019 (Update)

Official interest rates remain unchanged at 1.50% as we outline in detail below. Downgrades to growth and inflation forecasts in the RBA’s latest Statement on Monetary Policy were more substantial than we expected, the tone and language both more downbeat.

Whilst it is unlikely we will see any official rate movement for some time, funding costs for banks are changing constantly and this is being reflected in the ongoing changes to individual interest rate settings.

ME Bank, Macquarie Bank. NAB all adjusted variable rates up recently, whilst some of their fixed interest rates actually fell too.

--------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------

February 2019 (Rate Decision & Analysis)

At its first meeting for 2019, official interest rates remain unchanged at 1.50%.

So much happening in our economy at the moment, with a lot of change in sentiment alone since the end of 2018.

Globally, economic momentum has slowed markedly across the US, Europe and China. The trade tensions, higher interest rates and lack of confidence are among key factors in the slowdown.

Locally, lack of income growth for households, falling property prices have led to a fall to both consumer and business confidence which shows up in the weak GDP data.

As the money markets show below, sentiment has changed very quickly. The previous growth forecasts for the Australian economy look optimistic in many people's eyes, with many tipping that the next movement in interest rates could be a drop. This pressure is also exacerbated by another looming round of out of cycle interest rate increases for mortgages, as the second and third tier lenders catch up to the majors that moved some months ago.

Despite these local pressures, this author for one hopes that the RBA holds the line. At a time when global interest rates are increasing, the Australian economy needs to keep some monetary policy buffer up its sleeve to protect against a prolonged economic downturn should one occur.

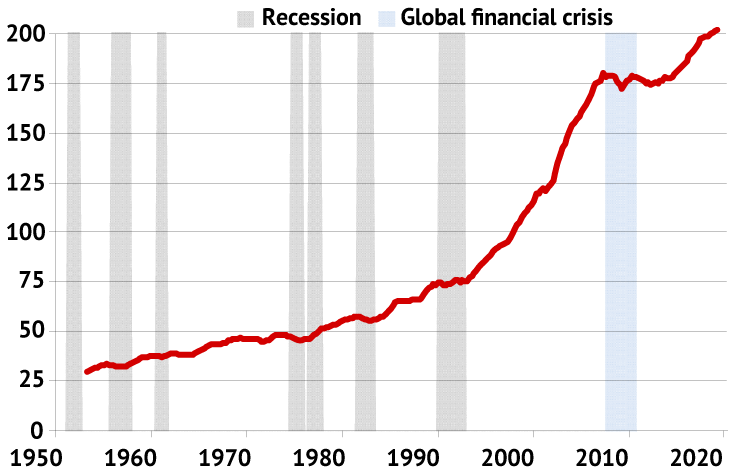

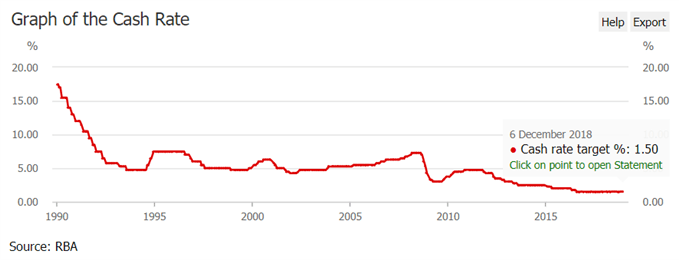

To put our interest rate position into context, the graph below from the RBA shows the long term history of the official cash rate, and a reminder of the diminished ability to provide economic relief via monetary policy.

Money Markets

On the money markets, short term rates have nudged up whilst long term rates are on the slide. The "spread" between the 180 Day and 10 Year rate averages around 75 basis points (or 0.75%); however, the recent period has seen this gap shorten to around 20 points. This is known as a flattening yield curve.

[table id=6 /]

As we have raised previously, if a small gap such as this continues for a sustained period it typically means expectations of weak economic conditions ahead. This means that there may be no immediate benefit to investing in long-term securities over short-term securities, since the return on either is similar.

There was a similar pattern back in 2016 which did not sustain, and many argue that in the current low interest rate environment this historical measure is less relevant. Not so sure.

Currency & Property

The AUD has been surprisingly robust (well, let's ignore the yo-yo during the last month) after the U.S. Federal Reserve signalled that it may slow the pace of interest rate increases. Robust commodity prices have also been a supporter for the Australian economy too.

After a 3 year spell (2013-2016) where the Aussie fell over 30% against the USD, we have had relative stability over the last three years. The AUD /USD currently sits close to its long term rolling average of 73 cents. For a currency that is the 5th most traded in the world, some would say a period of stability is welcome relief.

With tight credit, a looming election and generally negative sentiment, Property continues to be very weak. In fact, there have been 16 consecutive months of falls on a consolidated basis.

CoreLogic data below shows the declines in Sydney & Melbourne in particular, with both trending to over a 10% fall from previous highs.

Houses have been the hardest hit. To put the figures in another context, the medial price of a house in Melbourne has fallen from around $850,000 to $740,000 currently over the last year.

This of course needs context, as previous increases were unsustainable. It is also a sobering (and perhaps necessary) reminder that whilst people are generally emotional about property, at the end of the day it is another asset class that is subject to the power of the economy.

There still remains a number of downside risks to property, with further falls expected. Another significant factor is the relatively low level of turnover, meaning vendors are not having to really test the market. A key consideration here is job security. If employment is robust enough it will put a floor on prices ultimately.

We are in a new year that is full of uncertainty for a number of reasons.

--------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------

December 2018

At its final meeting for 2018, official interest rates remain unchanged at 1.50%.

With no meeting scheduled in January, markets get a chance to run without the yardstick of policy direction.

Despite a strong tally on the Australian Stock Market yesterday, other financial data across housing, GDP and employment has been slightly weak. With weaker house prices and tight credit conditions expected to continue, some economists are suggesting that the RBA's next move could be in fact be down. Especially if the negative sentiment is a further drag on consumer spending.

We still hold the view that this is an unlikely scenario, and it will be a very sluggish state of affairs for the economy if that in fact is the case.

The US story is one of caution, as their interest rate cycle coming to a "neutral" setting with another rate rise anticipated this month. The benchmark 10-year bond rate has also tapered off at the same time, so a flattening yield curve. This has prompted some commentators to look at history, along with other data, to predict a recession in the medium term. If that does occur, this more neutral rate setting will give them some headway to use if it is needed.

For Australia, we may have to define a new "neutral" for interest rates if the state of play continues into 2019.

Money Markets

On the money markets, nothing happening at all. In fact one of the least volatile periods we have seen in terms of rate movements as we reach the close of 2018.

Longer term money 3, 5 and 10 year Government Bonds very similar with only a small softening of the 10 year rate worthy of note.

[table id=4 /]

As we have highlighted for the past few months, the U.S. corresponding 10 year rate remains at a substantial premium though this divergence is starting to narrow a little as the graph below shows.

In terms of any potential global influence, the U.S. long term rates will be worth keeping an eye on going forward.

Currency & Property

The AUD has sustained its mini rally strengthening against the USD over the month. This is even more surprising considering interest rate divergence, and is partly the result of easing trade tensions between the U.S. and China.

The Property story continues to be bearish.

The latest data from Property experts CoreLogic below shows the continued soft results for Melbourne, Perth & Sydney in particular.

Anecdotally, we are seeing this weakening spreading to the middle and outer rings of the cities, with several valuation or vendor expectations at sale not being met.

More and more, property markets are very diverse by city and by region. Clearance rates are low, partly as many vendors are able to "wait it out" in the hope that the current weakness disappears.

The coming months will tell a story with some experts predicting there is more weakness to come.

--------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------

November 2018 - RBA Statement of Monetary Policy

"The Australian economy is performing well". This comment led off the RBA's November Statement of Monetary Policy which shows a positive tone. Further it states, "GDP growth is now expected to be around 3½ per cent on average over 2018 and 2019."

The overriding expectation is that we expect some upward movement in the medium term. Again the RBA stated, "The Board is expecting further progress in reducing unemployment and ensuring inflation is consistent with the target. If that progress is made, higher interest rates are likely to be appropriate at some point. However, given the expected gradual nature of that progress, the Board does not see a strong case to adjust the cash rate in the near term."

We hold our view that the next move will be up.

--------------------------------------------------------------------------------------------------------------------------------------------------------------------------------

Official interest rates remain on hold at 1.50% for November 2018.

This result is not a surprise of course. By comparison, the Canadian cash rate equivalent increased by 25 points to 1.75% and their tone is around the need to bring interest rates to a more "normal" level.

We have highlighted the weakening relevance between monetary policy in the U.S. and Australia. The same argument could be said for Canada too as we align ourselves more closely with Asia - China in particular. Though we raise it here as Canada's economy has a lot of similarities to Australia. Specifically in terms of its income profile and their high levels of household debt, so the impact of rate rises there on local conditions will be a litmus test of sorts for the RBA here.

The US remains a different story. The benchmark 10-year bond rate over the last month has been at it highest level for seven years, based on a continued bullish outlook for the performance of the local economy and the Federal Reserve turning its attention to making sure that inflation stays under control. This is despite the ongoing trade tensions and some downside risks with a softening equities market.

Currency & Property

Against this, The AUD has been surprisingly robust in fact strengthening against the USD over the month. This is based on a range of factors, including hope that the U.S. and China can reach some middle ground on their trade talks.

Again, locally the stable AUD is more mitigation for the RBA not to increase interest rates.

The Property story continues to be weak, yet divergent.

The latest data from Property gurus CoreLogic below shows the story of Melbourne following Sydney's slowdown. Perth continues its struggles.

Listings are down in capital cities as vendors wait it out in some cases, and new home sales are at very low levels. More and more, property behaviour is showing more distinctive segmentation across regional areas and capital cities.

The broad brush analysis doesn't cut it anymore so buyers and sellers need to be very well informed, so peel back from the layers from the data such as the above to help you in your decisions.

Money Markets

On the money markets, short term money were very inactive. We haven't seen any material movement at all since August this year, the positive is that helps the banks with their funding cost pressures.

Same story with long term money 3, 5 and 10 year Government Bonds hardly moved which is perhaps a welcome change from their volatility of the last six months. Again, the U.S. corresponding 10 year rate remains at a substantial premium (more than 50 basis points) and this remains a critical watch point.

[table id=2 /]

For further insights on interest rates, the RBA will release its Monetary Policy on November 9. This Statement presents an update of the their forecasts over the next two (2) years which will provide insights into where we are heading. Most commentators including this one expect that the next move will be up, though there is a lot of debate about when that could happen.

In an increasingly political environment, we will watch with interest how the coming months unfold.

Lastly, NAB have made the bold step of increasing variable interest rates, though only for new customers. This will reward existing customers which is a change in mortgage pricing strategy, clever.

-----------------------------------------------------------------------------------------------------------------------------------------------------------------------------------

The Reserve Bank announced after its monthly meeting today that official interest rates will remain on hold at 1.50% for October 2018.

Whilst rates are on hold here not so overseas. The U.S. cash rate equivalent increased again by 25 points to 2.25%. It followed a number of central banks in Europe which had similar increases over the last month. The US unemployment also rate fell to 3.7% in September, the lowest rate since December 1969 which outlines the strength of their economy.

Yes it is a very different financial world now, though the gap between U.S. and Australian central bank rates is now at its highest level since meaningful statistics were maintained. The RBA have stressed that monetary policy is not hinged to events overseas. This policy stance is fundamentally a good one, though perhaps convenient during an environment when we are not concerned about the impact of a lower Australian dollar.

On currency matters, the AUD has been stronger than most people would have thought in the last month or so buoyed by commodity prices. This arrests a 10% fall since the start of the year, mitigation to a low interest rate policy setting we enjoy currently.

So the point of all that commentary? I just can’t get my head around such a gap in interest rates between Australian and the U.S. So longer term, schoolboy economics says that interest rates will either be under upward pressure, or the AUD will depreciate against the USD.

This may also test the growing economic theory arguing a weakening relevance of our financial relationship with the U.S.

Markets

On the markets, short term money markets it is again an interesting time. We talked previously about a flattening yield curve. This will pause some of the pressure on bank funding costs for now, as the higher interest rates on mortgages we have seen in recent months settle in.

The upward momentum was with 3, 5 and 10 year Government Bonds which continued with their relative volatility with a near 20 point increase this month. Again, the U.S. corresponding 10 year rate remains at a premium.

Much of the broader economic data; including inflation, GDP, employment is relatively solid.

In an increasingly political environment, we will watch with interest how the coming months unfold.

-----------------------------------------------------------------------------------------------------------------------------------------------------------------------------------

The Reserve Bank left the cash rate unchanged at its September 2018 meeting today.

It has been a busy month, with the Royal Commission overhang (see related article) and the political events keeping banking in the spotlight.

Whilst rates are unchanged, and as I keep repeating, the role that monetary policy is being left for others. Amongst the loudest noise is the Westpac decision to raise variable mortgage rates out of cycle by 0.14% or 14 basis points, citing increased funding costs as their pressure point.

Westpac are the first major to act in this cycle, though the second tiers went some time ago, so we should not be surprised. I find the commentary fascinating and generally based on the emotion of large bank profits. Yes, it is unfortunate for those borrowers impacted. Though thinking it through, most would agree that banks should be commercial businesses that operate in a competitive market place. Perhaps another option is a return to Government owned banking?

Ironically, some have also criticised the major banks for absorbing funding costs increases to date, squeezing smaller financiers out of market share.

Most people would agree that all businesses (large or small) have the right to make decisions in the best interests of their shareholders. If they do not, the profits that the same mortgage holders rely on (generally via their superannuation) will diminish too and listen for the complaints if that happens.

Funding Costs

OK, emotions aside, what is meant by funding cost pressures?

For background, banks have diverse funding bases, with the primary ones being sourced from deposits, short-term & long-term wholesale debt and equity. We have seen a significant shift to internally generated deposits since the GFC, largely in response to a reassessment of funding risks by banks globally.

Deposit sourced funding now sits at over 60% of the total funding mix, and as we know there is always competition to attract deposits.

We always show bank bill swap rates each month (i.e market driven rates) and they are a relevant driver of this funding mix. These rates are the primary short-term reference lending base rate used in debt capital markets. As you have seen below, these now sit close to 50 basis points higher than the official cash rate, compared with a historical premium of around 20 points.

In simple terms, with a myriad of other inputs aside, the funding cost argument has merit.

Markets

Perhaps ironically in the context of funding costs, short term rates were very inactive over the last month. Exchange rates continue to soften which for some is a concern (Exporters excluded!), with the dollar touching its lowest level since January 2017.

The primary cause of this is a range of international factors that include uncertainty over trade agreements and the currency crisis that is impacting emerging markets. For the very brave, you can get a 60% return in Argentina on your deposits right now.

The RBA will welcome an inflation rate that at just over 2% creeps into its target range. The issue of household debt remains in the spotlight and so the pressure to keep a steady state of affairs.

So on the markets, the 10 Year Bond slide takes us back to the levels of the start of the year as the following table shows:

[table id=1 /]

Even without movement in central bank interest rates, other factors will stress test our economy in the medium term. This includes the cycle of interest rate increases, more stringent access to credit and higher amortisation of debt.

The spread between U.S. and Australian rates also continues to widen, which is a reminder that international events can impact us locally.

Just putting it out there, maybe an actual rate increase would have been better than all the punitive measures, and keep us in touch with the free market.

-------------------------------------------------------------------------------------------------------------------------------------------------------------------------------

AUGUST 2018

The Reserve Bank left the cash rate unchanged at its August 2018 meeting today.

Much of the role that monetary policy would normally play is being delivered in other ways. With weaker residential property markets (Note: Anecdotally it has been significantly softer over the last month) and the reduced availability of credit offsetting the short term need to raise interest rates.

The RBA will be hoping some wage growth comes and that it does so soon. Exchange rates are still a factor too. Our dollar is now 10% of its January 2018 levels, as it sits on its long term average of around 73 cents. So, good for now.

The reality is that rates overseas are on the rise with a range of factors impacting that. Central Banks such as India have raised rates again - now up to 6.50% - amid concern around currency stability and inflationary pressure. The U.S. has taken a short pause but more tightening is expected in the medium term.

The need to sit on this historically low setting based on local issues is compelling, especially if the focus is purely on domestic implications. Though this may ultimately be taken out of our hands.

On the markets, more yo-yo activity and we are largely back to where we were in June this year as the following table shows:

[table id=1 /]

As we introduced last month, the spread between the 90 Day and 10 Year rate is at 75 basis points (or 0.75%), the average over the last five years. In short, things look reasonably normal or the "new" normal, especially from that interesting period in August 2016.

In terms of funding costs and lending, the "Empires Strike Back" with majors ANZ, CBA reducing a selection of interest rates as they target stronger banking customers. This comes at a time where smaller and regional lenders have had to increase their mortgage rates citing rising wholesale funding costs, and the small thing of a Royal Commission too.

The volatility in rates for borrowers will continue for a while yet and with the focus on regulatory, compliance and other prudential controls expect the world of finance to become increasingly complicated in its application.

------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------

JULY 2018

The Reserve Bank left the cash rate unchanged at its July 2018 meeting today.

The placid sentiment amongst some economists and the central bank is pushing out expectations of any official interest rate rise in the medium term.

It is now almost two years since the last rate change. On one hand, many macro economic data indicators (including low unemployment, improving deficits, inflation within target etc.) tell a good tale. The RBA should be commended for the part it has played in keeping our finances in solid shape over this historcial period.

However, an argument to remove this sustained period of low rates is growing in momentum, especially if you hold the view (as this writer does) that the cash rate is a key plank for setting monetary policy.

Market rates and bank funding costs are on the rise, with the sustained increases in the U.S. having a big impact on our rates here. This means banks are raising their variable interest rates independently of the official cash rate.

If markets continue to rise, the risk is that the cash rate setting loses it relevance. Instead, there will be reliance on macro regulation as a complex and layered tool for providing the economic panacea.

Some experts, such as ANU Economist and former RBA Board member Warwick McKibbin, argue that it is better to move sooner rather than later "as a way of protecting Australia against the risk that the U.S. economic expansion overheats" and that we do not want "to be sitting on very low interest rates when the shock comes."

Good food for thought, perhaps this only becomes real when our currency finally drives lower than desired and the price of imports starts to impact inflation.

On the markets, we ended up with a flattening yield curve, which for many is cause for concern, though locally here not as pronounced as overseas as the following table shows:

Date |

Cash Rate |

90 Day Rate |

10 Year Bond |

| Aug 2016 | 1.50% | 1.79% | 1.82% |

| Aug 2017 | 1.50% | 1.69% | 2.66% |

| Dec 2017 | 1.50% | 1.75% | 2.54% |

| May 2018 | 1.50% | 2.05% | 2.82% |

| June 2018 | 1.50% | 1.98% | 2.70% |

| July 2018 | 1.50% | 2.12% | 2.63% |

For the historians, the average spread between the 90 Day and 10 Year rate has been about 75 basis points (or 0.75%) over the last five years. In short, things look reasonably normal or the "new" normal, especially from that interesting period in August 2016.

We will watch for the impact of any higher funding costs to creep into the price of debt.

------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------

JUNE 2018

The Reserve Bank left the cash rate unchanged at its June 2018 meeting today.

Increasingly, we are seeing the RBA make reference to more global factors, and the overriding theme is patience. The current setting is best for Australia's longer term prosperity despite some underwhelming data.