March 2023: Rate Decision & Economy

The Reserve Bank of Australia ("RBA") met today for the second time this year, raising the official cash rate by a further 0.25%. The momentum on market interest rates and strong commentary around inflation, meant the move had an inevitable look about it despite some softer local results.

Economic Sentiment

Consumer confidence remains subdued but to date households are still spending. However, GDP data from last quarter showed only modest growth and on an annualised basis dipped under 3% which was below expectations. It seems that "good" news these days can be in the form of factors that drive down inflation, so weaker than expected wage growth was a form of positive news for the local market.

This is the tightrope for the Government - how to achieve growth through a period of inflation and the requisite increase in interest rates it needs to dampen it.

Business Sentiment

As we mentioned last month, 'Business Confidence' remains cautious but relatively strong. Data from the Australian Bureau of Statistics showed that Australian businesses are planning to invest around $130 billion in capital expenditure in 2024 for example.

In part this is elevated by the rate of inflation, though it is still good resilience against rising interest rates and weaker forward data.

This said, many business leaders have been vocal about their expectations of a softer twelve months ahead, so perhaps investing with some caution.

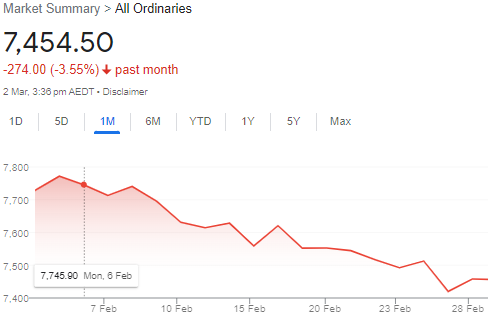

Shares & Markets

After a very strong run of late, sentiment has caught up with the Australian share market. A negative month in February for the All Ordinaries, falling by over 3%. This is perhaps not surprising given their 2021 highs.

The fall in Australian shares was reflective of a wider story worldwide, as investors are starting to worry again about the sustainability of the global economy.

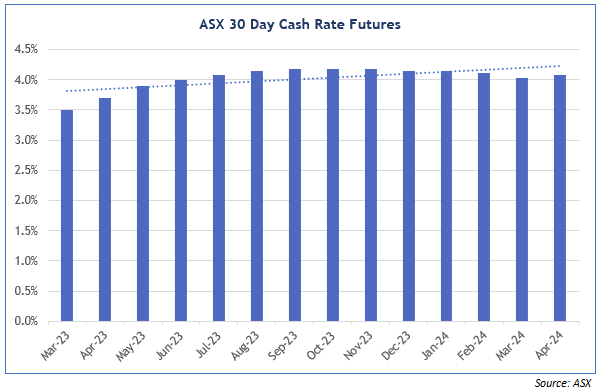

Direction for Local Interest Rates?

Again, some insights from the ASX Cash Rate Futures, gauging month to month expectations in terms of a destination for the peak cash rate. A sharp increase in expectations this month, with the market now conditioned for more rate rises before a softening in early to mid-2024.

This is indicated by the ASX Cash Rate Futures as below.

Financial markets are therefore implying that the cash rate will peak and hold at around 4.2% until April 2024.

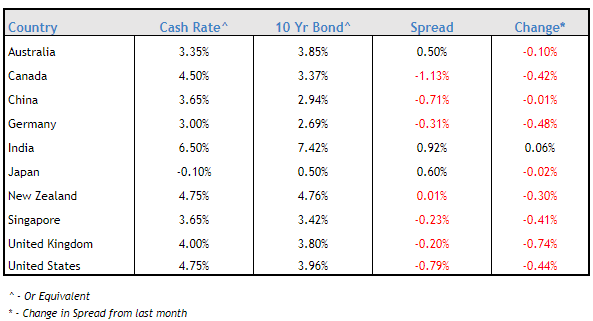

Update for Interest Rates Worldwide

Central banks across the developed world continue to deal with higher central interest rates knowing that their settings have strong consequences.

New Zealand remains a watch especially with severe weather events causing shorter term challenges. Their central bank meets in April where further rises are still expected. There also remains real concern about households, with 90% of mortgages currently on fixed rates and a lot of these coming off over the next 12 months.

In the UK, the Bank of England moved with another 50 point increase to 4.0% at their February meeting, the highest level in 14 years. While more rises are expected there is some optimism that inflation is near its peak.

The U.S. yield curve is now less inverted at the short end at least, with the 2 year sitting at close to 5% (15+ year high). This follows their very strong local data that means that the central rate will exceed 5.0% during 2023. This will mean a 25 basis point rise when the Federal Reserve meets later this month.

In Canada, after their eighth rate hike in this cycle last month, the consensus is that their central bank will hold at 4.50%. Their economy is one that seems at the front of the cycle, with prices and growth levels both stabilising.

In the Eurozone, the momentum has changed quickly, with central interest rate expectations to 4%, especially after inflation in France, Spain and other parts of the region increased more than expected.

Before posting any changes today, we compare central bank cash rates and their longer term 10 year bond yields. The "spread" has narrowed this month, with long term rates increasing significantly.

As a sweeping statement, this is reflective of expectations around higher interest rate expectations, with long term rates looking at a realistic setting in a more "normal" rate world.

The change or narrowing of the spread between short and long term money is one to watch from here on. Now that short term rates are higher and potentially more settled, we can see what the market thinks of the long term prospect for rates and economic conditions in the future.

Local Money Markets

Australian money markets were active, and yields rose across all terms.

The yield curve is very flat right now, though more "normal" than other economies. The RBA still has room to move if need be.

| Month | Cash Rate | 180 Day | 10 Year |

|

Apr 22

|

0.10% |

0.70% |

2.87% |

|

May 22

|

0.35% |

1.40% |

3.12% |

|

Jun 22

|

0.85% |

1.94% |

3.48% |

|

Jul 22

|

1.35% |

2.70% |

3.54% |

|

Aug 22

|

1.85% |

2.78% |

2.96% |

|

Sep 22

|

2.35% |

3.04% |

3.65% |

|

Oct 22

|

2.60% |

3.55% |

3.90% |

|

Nov 22

|

2.85% |

3.61% |

3.74% |

|

Dec 22

|

3.10% |

3.48% |

3.48% |

|

Feb 23

|

3.35% |

3.67% |

3.50% |

|

Mar 23

|

3.60% |

3.94% |

3.85% |

The 180 day rate jumped up as expected in line with changing expectations about higher interest rate rises.

The 10 year rate followed markets worldwide and moved materially (3 and 5 Year money moved even higher) as our yield curve goes flat. The market has changed its view of the severity of future interest rates and done it quickly.

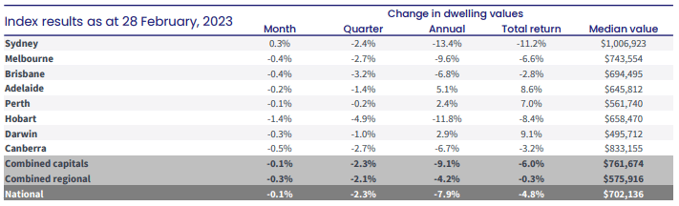

Residential Property

The latest residential monthly property results from CoreLogic show an overall fall, but more modest than recent trend, in fact Sydney actually recorded an increase last month.

Early days, though one headline is that consolidating housing values coincides with low supply levels and an overall increase in clearance levels.

Some really good residential property analysis was released in February from Charter Keck Cramer specifically around the Apartment market in Australia.

Many of the key insights were similar to sentiments we revealed last month, namely:

Population growth drives the demand for additional and diverse dwelling types. For example, Melbourne is very reliant on Net Overseas Migration ("NOM") and it will take the largest share of NOM in Australia (34%) over the next decade, with Sydney closely following on 32%. This will create upward demand.

There is a major rental crisis in many parts of Australia, as we know, and this is anticipated to remain for the next few years.

In summary, CKC envisage a "natural price floor on price falls of apartments", driven by the shortage of supply, higher rents, and despite a record level of longer term renters an inherent desire for many to buy.

Retail Property

Not surprisingly, the most maligned sector of the property market has been Retail.

So it was really encouraging to read that the Melbourne CBD led a really strong contraction in the vacancy rate to only 9.2%, only with some improvements in other markets (other than a struggling Perth with a vacancy rate of 26%). This was in part led by returning office workers and international students, and more conformation that our broader read of the economic conditions is patchy.

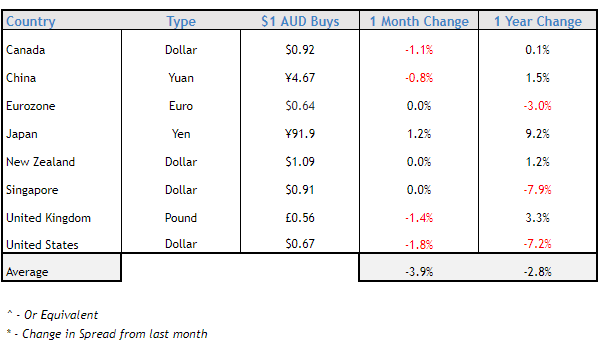

Currency

The Australian dollar fell to its lowest level this year, just below US68¢, as the strong US data meant it outperformed most currencies.

Otherwise it was a fairly steady month.

The AUD remains a relevant currency on world markets, in fact it is the 5th most traded currency in the world, behind the USD, Euro, Yen and Pound.

We wish you another prosperous month ahead.