December 2023: Rate Decision & Economy

The Reserve Bank of Australia (RBA) has today announced no change to the official cash rate, leaving it at 4.35%.

The yo-yo of sentiment continues. The highlight for the month was the CPI indicator, which rose 4.9% in the 12 months to October, down from a rise of 5.6% in September. The market hyped this a lot though the drop in inflation wasn’t broad based and there was less information on the services side which remains the prime area of concern.

Economic Results & Sentiment

It is hard to read the full picture. Immigration is certainly keeping activity strong, employment levels remain robust (despite recent wobbles) and property owners feel better when house prices are climbing.

Against this ANZ and ABS data showed that nominal retail sales fell month on month for October. Now growing at an annual 1.2%, this is the weakest annual result since August 2021. Perhaps the end of the year comes at a good time as markets can pause and get a chance to match sentiment with what is actually happening in the real world.

OECD & Australia

Last month it was the IMF saying Australia had to do more on inflation. This month the OECD clearly thinks we have done enough. They forecast GDP growth to slow to 1.4% in 2024, with rate rises and other cost of living pressures forcing households to cut back on spending significantly.

They also note that the economy will be buffered by Australia’s strong migration intake, which is relatively efficient in meeting the strong labour demand.

RBA Stance

With a rise at November's meeting, the RBA commentary remains robust on inflation and how the current settings are impacting different segments of the economy. A weakness of monetary policy being used as an economic tool?

New Governor Bullock echoed the sentiments of many in the market with a view that things are better than we may have expected.

"Despite that noise, households and businesses in Australia are actually in a pretty good position. Their balance sheets are pretty good,” Ms Bullock said.

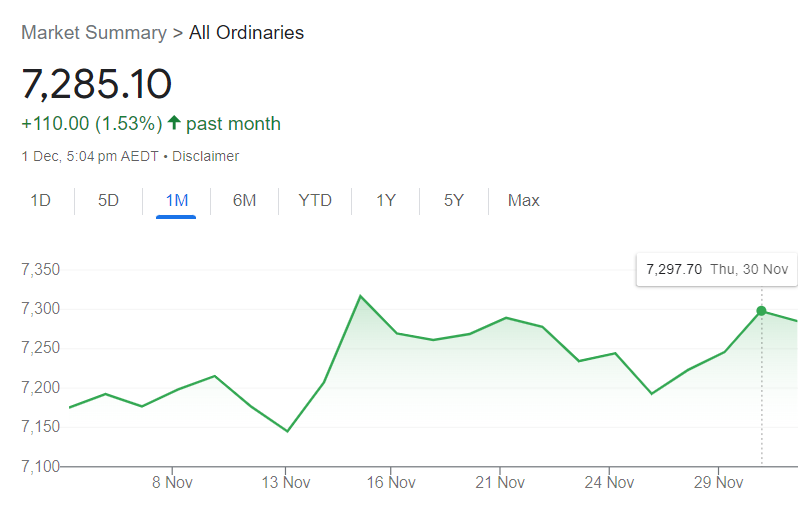

Shares & Markets

The market ended November, traditionally a good month for equity markets, with a rise in the All Ordinaries, reversing the losses from last month.

Well, reverse what I said last month. The sentiment changed after inflation fears subsided and bond yields fell.

The real story was the U.S. where markets rallied strong (7%) in November following three straight months of declines, based on expectations that the Fed was at the end of its monetary tightening campaign. Thankfully, this was also based on fundamentals including stronger than expected company earnings.

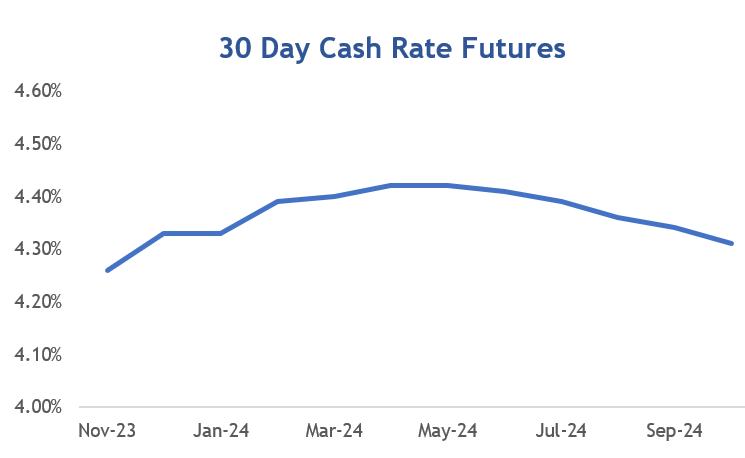

Direction for Local Interest Rates?

A month is a long time in hyper sensitive markets looking for direction.

No surprise then with a fall this month in the ASX Cash Rate Futures seeing a circa 15 point decrease in expectations. This takes us back to where we were two months ago indicated by the ASX Cash Rate Futures below.

Financial markets are now implying that the cash rate is close to peak and some falls are being priced in towards the back end of 2024. The RBA may end up looking okay into 2024, potentially holding ground on interest rates while other countries operating a rate premium will start to ease off theirs. Those championing a higher exchange rate would be pleased indeed.

Update for Interest Rates Worldwide

Major central banks across Europe, the UK and Americas were quick to hose down expectations they could soon pivot to cutting interest rates, saying the battle against inflation is unfinished and the risk of further tightening should not be dismissed.

New Zealand's central bank left the cash rate unchanged again at 5.50%; but noted inflation remained too high and that some policy tightening is not out of the question. This surprised markets as local conditions are pretty tough.

The U.S. stays at 5.50% rate with no meetings in between ours. Their message around monetary remains consistent. Chairman Powell said, “It would be premature to conclude with confidence that we have achieved a sufficiently restrictive stance, or to speculate on when policy might ease. We are prepared to tighten policy further if it becomes appropriate to do so." Markets ignored that message.

In the UK, the Bank of England kept rates on hold this month for the second consecutive meeting at 5.25%. Annual fell just below 5% which was cause for celebration (remember they peaked at 11%) and bond markets are already pricing in 2 to 3 cuts by end 2024. The central bank is cautioning them not to jump the gun.

Canada, remains at 5.00%, with greater confidence that their previous rate hikes are working to slow the economy and inflation.

Central Bank Cash Rates

Before posting any changes today we compare central bank cash rates and their longer term 10-year bond yields.

All the action this month is in the end of the curve, with the 10 year bond rate falling while short term rates remained virtually unchanged.

|

Country |

Cash Rate | 10 Year Bond | Spread |

|

Australia

|

4.35% | 4.49% | 0.14% |

|

Canada

|

5.00% | 3.45% | -1.55% |

|

China

|

3.45% | 2.70% | -0.75% |

| Germany | 4.50% | 2.35% | -2.15% |

| India | 6.50% | 7.29% | 0.79% |

| Japan | 0.00% | 0.71% | 0.71% |

| New Zealand | 5.50% | 5.10% | -0.40% |

| Singapore | 3.66% | 2.99% | -0.67% |

| United Kingdom | 5.25% | 4.14% | -1.11% |

| United States | 5.50% | 4.41% | -1.09% |

The majority of major economies have an inverted yield curve. This is defined as an interest rate environment in which long-term bonds have a lower yield than short-term ones.

Local Money Markets

Australian money markets reversed the trend of last month, falling as the chance of another rate rise dissipated. The 10-year rate reversed as it processed the world's view about interest rates (again).

| Month | Cash Rate | 180 Day | 10 Year |

|

Dec 22

|

3.10% |

3.48% |

3.48% |

|

Feb 23

|

3.35% |

3.67% |

3.50% |

|

Mar 23

|

3.60% |

3.94% |

3.85% |

|

Apr 23

|

3.60% |

3.81% |

3.30% |

|

May 23

|

3.85% |

3.82% |

3.34% |

|

Jun 23

|

4.10% |

4.21% |

3.65% |

|

Jul 23

|

4.10% |

4.67% |

4.03% |

|

Aug 23

|

4.10% |

4.70% |

4.06% |

|

Sep 23

|

4.10% |

4.37% |

4.02% |

|

Oct 23

|

4.10% |

4.41% |

4.48% |

|

Nov 23

|

4.35% |

4.73% |

4.72% |

|

Dec 23

|

4.35% |

4.58% |

4.49% |

Gut feeling is that we have these settings about right locally. It may be good timing if the rest of the world eases monetary policy dramatically over the next 18 months and Australia takes a more modest approach.

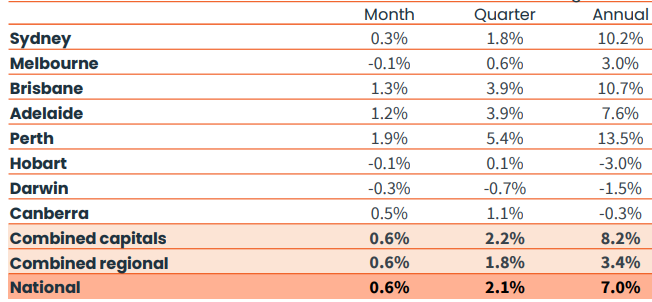

Residential Property

The latest residential monthly property results from CoreLogic showed a 0.6% increase during November, with the smallest monthly gain since February, still relatively robust.

The strength continues to sustain in boom markets Adelaide, Perth and Brisbane. These cities continue to outperform the other capitals. Sydney and Melbourne were the softest for some time so that is a watch.

Commercial Property

There is mixed sentiment across other property sectors. The soft office market (especially at the larger end) is starting to really hurt as a combination of weak income and capital values impact fund valuations. Losses are now being booked recognising the lag in these long term assets.

Vacancy rates remain high and above trend. There is a clear strategy of incentives for tenants (around 40%) but as new stock won't be in real volume over the coming period, keeping "face" rents strong may leave landlords in a better position in the long run.

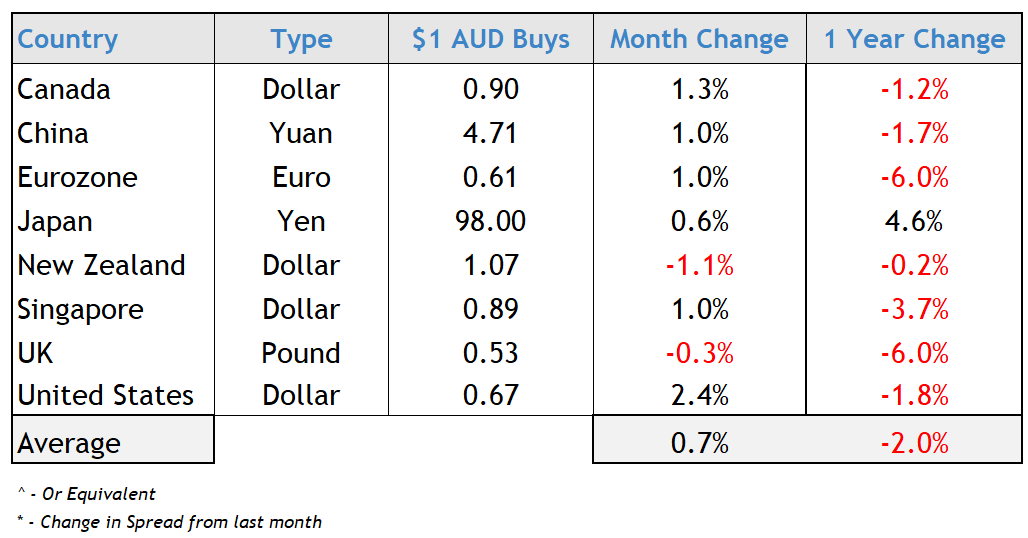

Currency

The Australian dollar went on a well hyped strengthening against the USD, though as the data shows it was much more benign against other major currencies.

There are a number of factors supporting our dollar including strong commodity prices (iron ore) and the impacts of last month's rate rise. However, the Australian dollar remains sensitive to interest rates and news from China as our biggest customer of commodities.

As this is our last Economy & Property post for 2023, we wish you every success and best wishes in the run up to Christmas and 2024.