April 2022: Rate Decision & Economy

The Reserve Bank of Australia ("RBA") met for April, leaving the official cash rate unchanged at 0.10%.

Markets all over were busy this month.

The US economy is very hot, with inflation reaching a 40-year high of almost 8%. This was led by increasing gas, food and housing costs. The impact of the war in Ukraine is obviously fuelling some of these pressures.

Bond Markets went crazy, whilst in the Equities Market here was also a little stronger than expected.

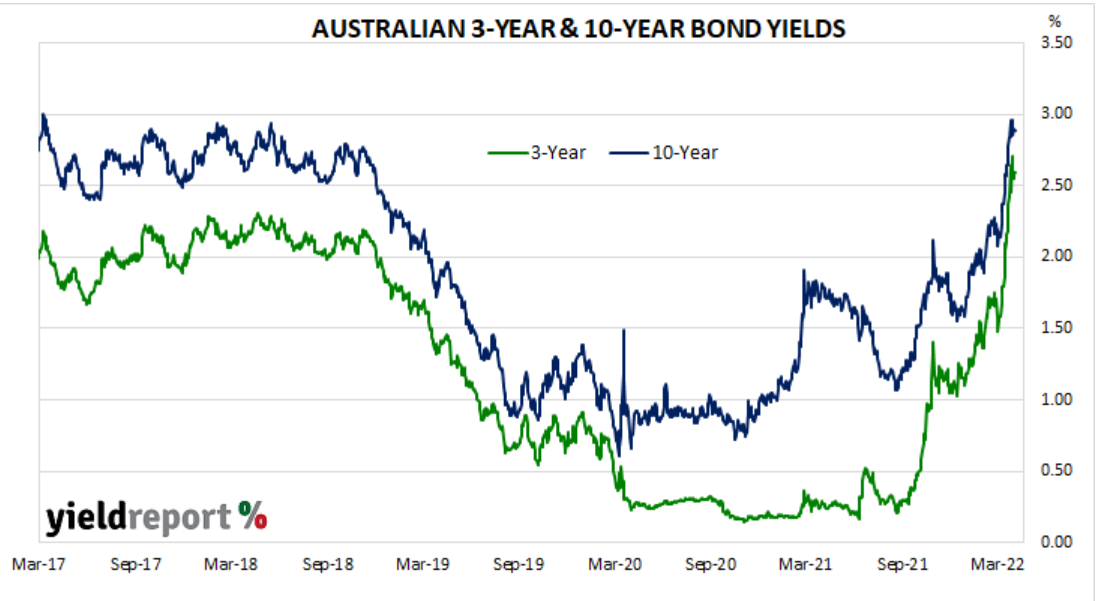

Short & Medium Term Money Is Up

The benchmark Australian 3-year bond yields jumped materially this month and to its highest point since 2014, now well over 2%. This rate correlates strongly to short-term interest rate expectations and the Yield Report data below demonstrates its rapid ascension.

This follows the trends of other markets worldwide.

Why are Bond Yields Important?

We talk a lot about bonds and money markets in the context of economic performance. This is because the yield curve for bonds is an important indicator in financial markets. It helps to determine how actual and expected changes in the official interest rate, along with changes in other factors, feed through to other interest rates in our economy.

It is also a barometer for investors' expectations for future economic growth and inflation.

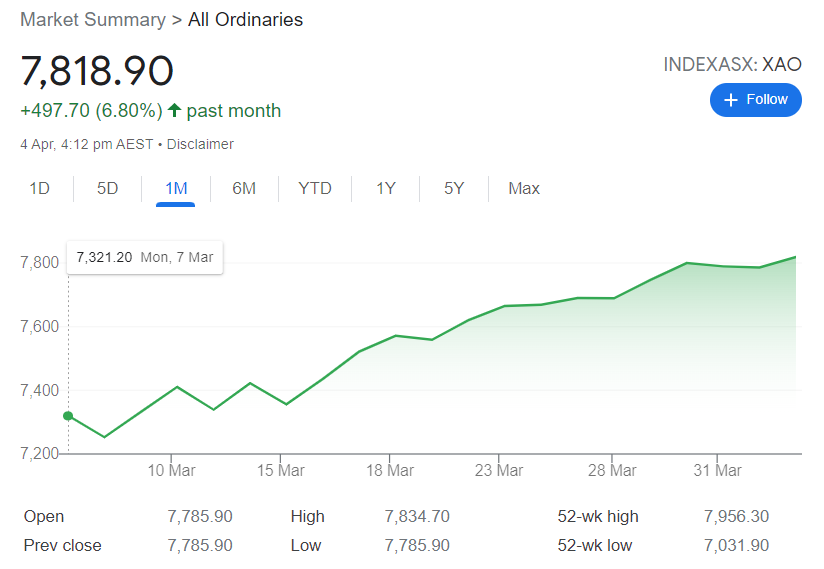

Shares & Markets

Over the month, the Australian share market was in very positive territory as indicated below:

Despite rapid increases in bond yields, both the US market and our local market shook off concerns and focused on more positive economic news.

The ultimate test will be once higher interest rates eventuate and the impact on the broader economy is tested more broadly.

Direction for Interest Rates?

North.

I really feel for the RBA right now. The impact of inflation and the movement of central banks worldwide, has created a scenario where they must do something to curb demand.

The RBA is very wary that as rates climb, increased mortgage repayments will impact households hard on top of rising prices for necessities such as utilities, fuel and groceries.

The RBA is not convinced that recent spikes in petrol prices and like items, will sustain and drive sustained inflation. Their last minutes confirmed, "The Board will not increase the cash rate until actual inflation is sustainably within the 2 to 3 per cent target range. While inflation has picked up, it is too early to conclude that it is sustainably within the target range."

The USA are finally off to the races. After raising interest rates by 25 points and signalling several more increases this year, Federal Reserve Chairman Mr Powell sees the challenge of high inflation and a tight labour market as real concerns.

Money Markets

This was a really busy month on money markets as we said, with an increase in yields not seen for some time.

Markets are well and truly away now.

| Month | Cash Rate | 180 Day Bill Rate | 10 Year Bond |

|

May 2021

|

0.10% | 0.04% | 1.65% |

|

June 2021

|

0.10% | 0.04% | 1.59% |

|

July 2021

|

0.10% | 0.07% | 1.48% |

|

August 2021

|

0.10% |

0.05% | 1.12% |

|

September 2021

|

0.10% |

0.04% | 1.18% |

|

October 2021

|

0.10% |

0.05% | 1.45% |

|

November 2021

|

0.10% |

0.20% | 2.09% |

|

December 2021

|

0.10% |

0.14% | 1.93% |

|

February 2022

|

0.10% |

0.26% | 1.98% |

|

March 2022

|

0.10% |

0.27% | 2.22% |

|

April 2022

|

0.10% |

0.70% | 2.87% |

The 10 year rate jumped around but ended up 65 points higher over the month, the highest since November 2018, largely on inflation concerns and the likelihood of rising interest rises. This kept the yield curve relatively normal as other short term rates climbed significantly on the back of these expectations.

In the US, the bond market showed brief signs of the dreaded inverted yield. Their 10-year Treasury bond dipped below that of the 2-year benchmark bond.

As we have discussed previously, an inverted yield curve (i.e. where short-term bond yields are higher than long-term bond yields) is a traditional indication that recessionary conditions are on the horizon. With markets so crazy right now, best not to draw any conclusions until things settle down.

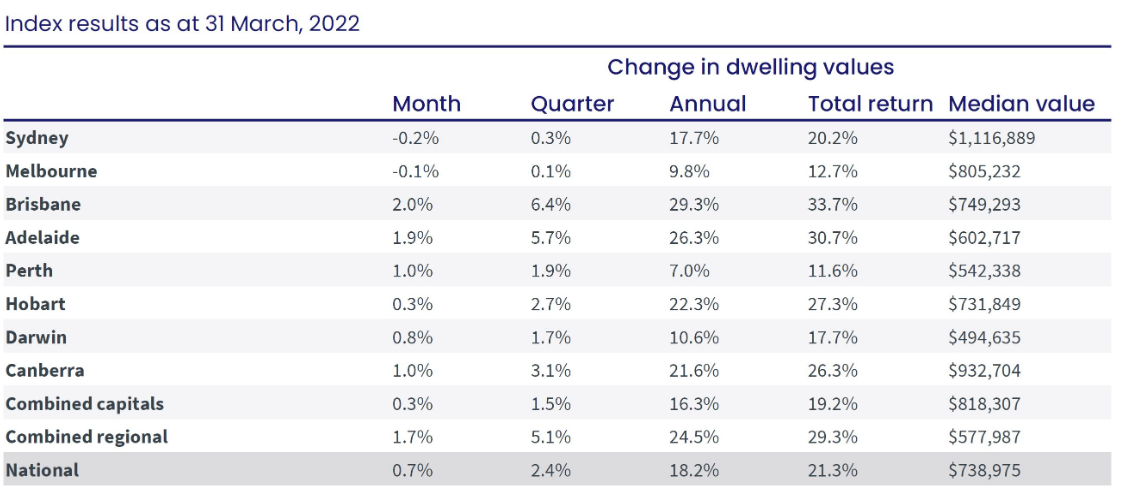

Property

Whilst Australian housing values have been tested over the coming months, the first quarter of the year has seen Australian dwelling values rise by "only" 2.4%, the lowest in some time.

CoreLogic data below shows us that the slowing of growth is manifesting its way into the data.

Sydney and Melbourne's growth rate is showing the most significant slowdown, falling to 0.3% and 0.1% in the first quarter of 2022 respectively.

Regional Australia maintains its recent growth and is still trending ahead of cities.

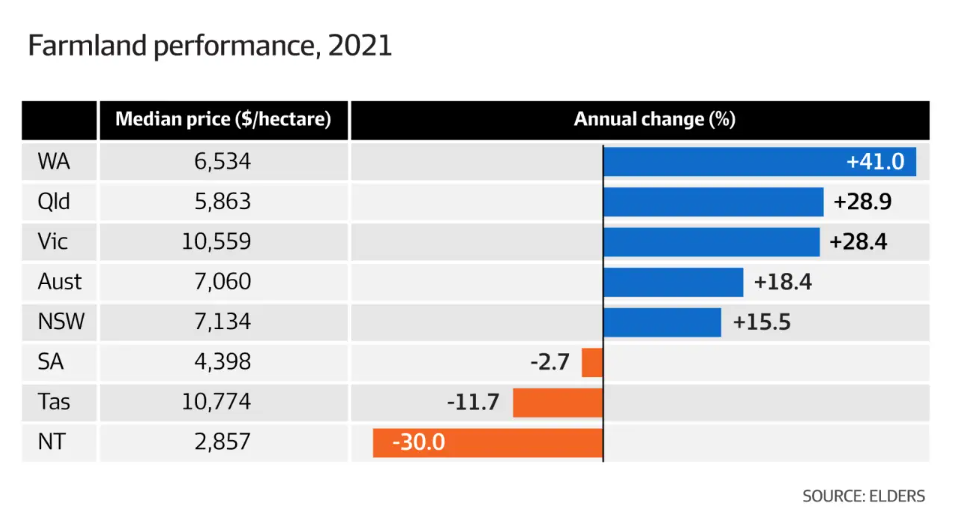

Continuing the Regional themes, recent data from Elders demonstrated the significant increase in demand for Agri property last year in most markets - and demand continues into 2022.

The report showed that Western Australia was driven by the strength of the grain industry, whilst other markets in NSW and Victoria were more driven by lifestyle factors as contributors.

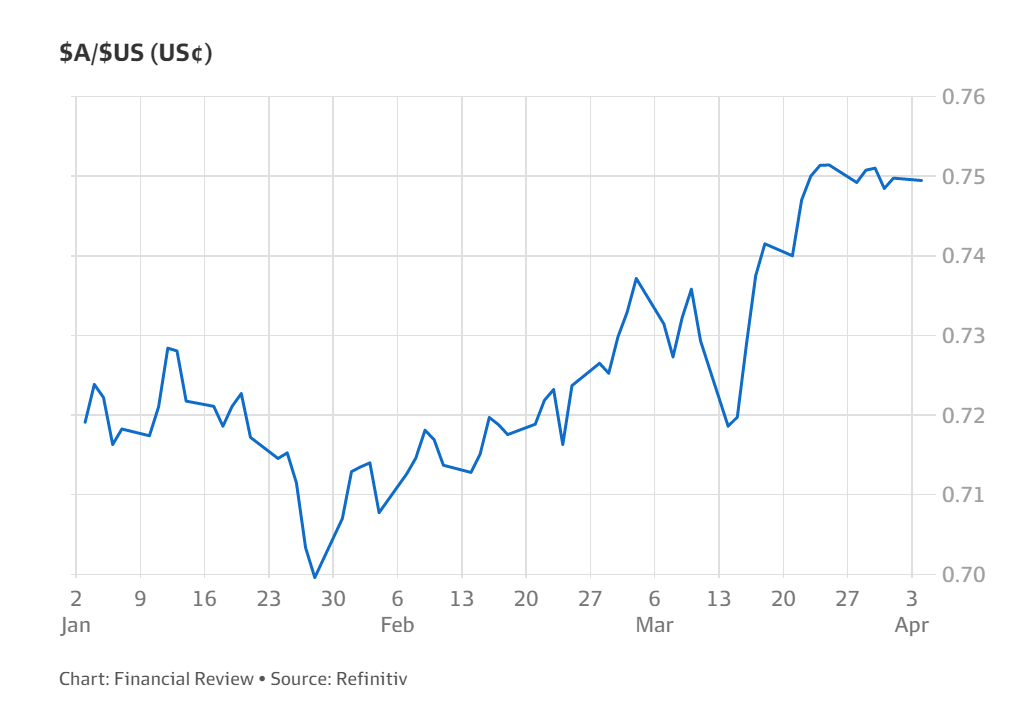

Currency

The likelihood of higher interest rates and commodity prices has given a boost to our currency, and surprisingly, the Australian dollar increased by around 3% during the last month.

Refinitiv/Financial Review data shows that this is the second-largest monthly increase since January 2021.

Until next time.