As we move away from emergency settings for monetary policy, interest rate increases are inevitable.

We have seen a dramatic rise in short and long term market rates. Other economies - both large like the USA and local such as New Zealand, have acted swiftly and aggressively to thwart inflation and asset price growth.

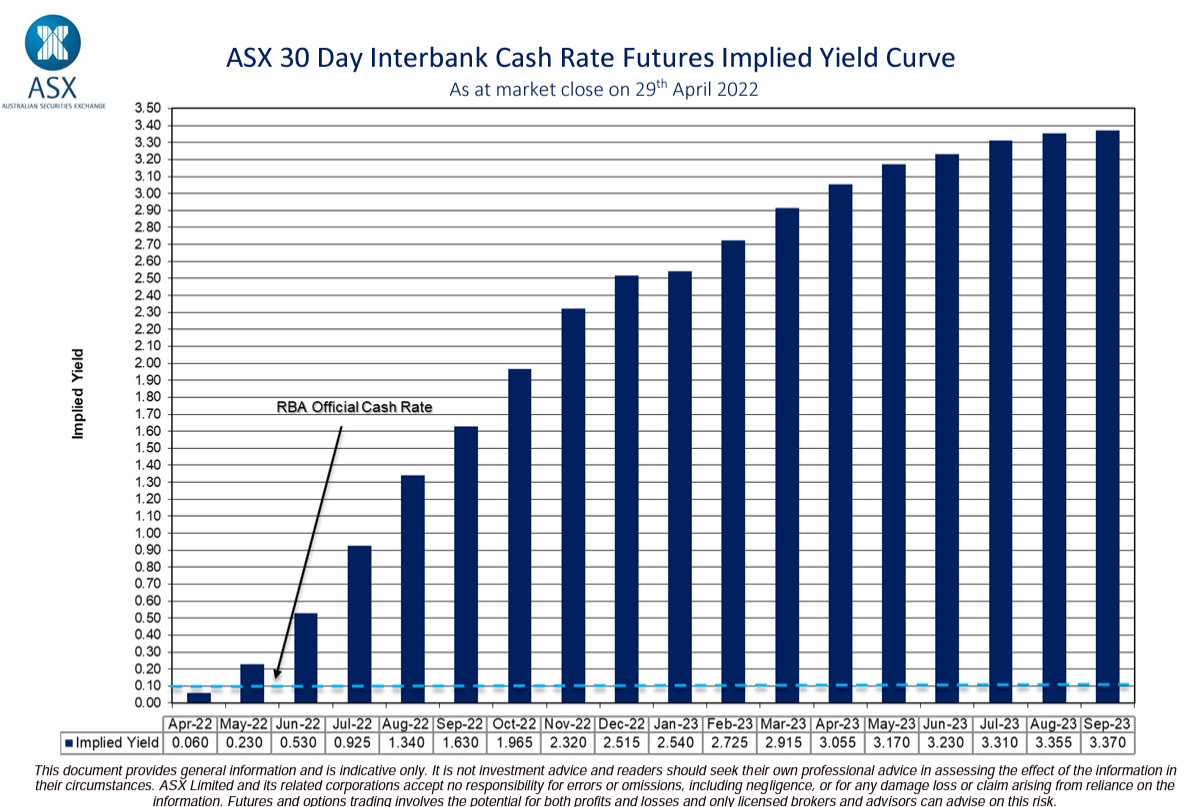

What will the Reserve Bank Do?

How much the RBA jumps initially is not clear. It is either death by a thousand cuts or some bigger rises to catch up to the market expectations more quickly.

Looking at markets, they are pricing in a rate increase in the medium term of more than 2.5% (or 250+ basis points). These predictions include indicators like the ASX Cash Rate Futures as below:

Looking at RBA commentary, not sure they would agree with this level of rise, at least until there is sustained growth in wages. In their eyes it is a wait and see.

In terms of building expectations over the coming period, another option is to look at models as opposed to sentiment based indictors above.

As fixed mortgage interest rates increase, the gap between variable and fixed rates provides direction on where variable mortgage rates could end up. As an average, variable rates sit around 60 basis points lower than the prevailing 3 year fixed rate.

By this albeit crude measure, that means a total rise of around 150 basis points in this period.

Should I Fix Interest Rates Now?

If you are looking for fixed rates, we feel that ship has sailed. For example, a recent 250 basis point increase in 3 year money has seen banks react swiftly. Presently, the average 3 year fixed mortgage is priced about right - with a margin of around 170 basis points over the respective wholesale rate the norm over time.

The statistics tell us that the borrower loses most of the time on fixing interest rates (more than 80%). This can be from moving too early, or more often too late in the rate changing cycle. It is also because financiers need to win because of the risk they are taking too.

For monthly intervals between 1990 to 2019, you would have been better off taking a 3 year fixed rate only 13% of the time. Looking further into this data there have only been four clusters of months when you would have been better off, though in 2.5 years' time we will add a fifth.

How will Banks React?

Whilst competition remains strong, with rates for variable loans holding; funding costs are biting for banks and an increase in the official cash rate will be a relief for lenders.

It is helpful that domestic deposits, thanks to Government stimulus, now represents over 60% of funding composition for the majors, with banks not testing markets with issuing any new bonds.

However, increases will be passed on (very) swiftly. In competitive markets, lenders will make changes "out of cycle" (i.e. greater or less than the RBA move) to re-set their positioning.

How can I prepare for Rate Rises?

In the past, for many finance advisers the discussion used to be centred around scenarios. "How will it impact you if interest rates increase by 2%?". Well, this is relevant now.

The preparation should primarily focus on:

- Sensitise all your borrowings at a buffer of 2.5% now. See what the cashflow impact is and plan accordingly.

- Consider whether you can retire more debt whilst interest rates are lower, reducing future pressure to cash flow.

- Consider whether you can restructure or refinance your borrowings to different products which have lower interest rates.

Looking in Hindsight

So what else does history tell us?

Markets generally have a weak track record of predicting interest rate movements. So hopefully 250 or 300 points doesn't land on our doorstep too soon.

More Information?

E - enquiry@mcpgroup.com.au We can provide a scenario calculator to test the impact of higher interest rates.

The team at MCP Financial Services has specialised expertise in supporting your business and personal finance requirements.

The information in this article is general information only. It is not intended to be a recommendation or constitutes advice.